Wells Fargo 2013 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2013 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

initiated process upon discovery of the uninsurable loan (usually

within 180 days from funding of the loan). Alternatively, in lieu

of repurchasing loans from GNMA pools, we may be asked by

FHA/HUD or the VA to indemnify them (as applicable) for

defects found in the Post Endorsement Technical Review

process or audits performed by FHA/HUD or the VA. The Post

Endorsement Technical Review is a process whereby HUD

performs underwriting audits of closed/insured FHA loans for

potential deficiencies. Our liability for mortgage loan repurchase

losses incorporates probable losses associated with such

indemnification.

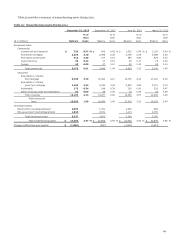

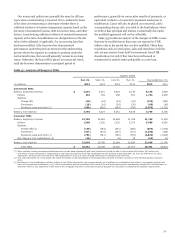

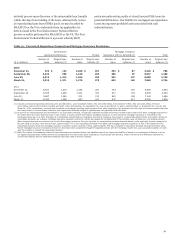

Table 39: Unresolved Repurchase Demands and Mortgage Insurance Rescissions

Government

sponsored entities (1) Private

Mortgage insurance

rescissions with no demand (2) Total

($ in millions)

Number of

loans

Original loan

balance (3)

Number of

loans

Original loan

balance (3)

Number of

loans

Original loan

balance (3)

Number of

loans

Original loan

balance (3)

2013

December 31, 674 $ 124 2,260 $ 497 394 $ 87 3,328 $ 708

September 30, 4,422 958 1,240 264 385 87 6,047 1,309

June 30, 6,313 1,413 1,206 258 561 127 8,080 1,798

March 31, 5,910 1,371 1,278 278 652 145 7,840 1,794

2012

December 31, 6,621 1,503 1,306 281 753 160 8,680 1,944

September 30, 6,525 1,489 1,513 331 817 183 8,855 2,003

June 30, 5,687 1,265 913 213 840 188 7,440 1,666

March 31, 6,333 1,398 857 241 970 217 8,160 1,856

(1) Includes unresolved repurchase demands of 42 and $6 million, 1,247 and $225 million, 942 and $190 million, 674 and $147 million, 661 and $132 million, 534 and

$111 million, 526 and $103 million and 694 and $131 million at December 31, September 30, June 30 and March 31, 2013, and December 31, September 30, June 30 and

March 31, 2012, respectively, received from investors on mortgage servicing rights acquired from other originators. We generally have the right of recourse against the seller

and may be able to recover losses related to such repurchase demands subject to counterparty risk associated with the seller.

(2) As part of our representations and warranties in our loan sales contracts, we typically represent to GSEs and private investors that certain loans have mortgage insurance to

the extent there are loans that have loan to value ratios in excess of 80% that require mortgage insurance. To the extent the mortgage insurance is rescinded by the

mortgage insurer due to a claim of breach of a contractual representation or warranty, the lack of insurance may result in a repurchase demand from an investor. Similar to

repurchase demands, we evaluate mortgage insurance rescission notices for validity and appeal for reinstatement if the rescission was not based on a contractual breach.

When investor demands are received due to lack of mortgage insurance, they are reported as unresolved repurchase demands based on the applicable investor category for

the loan (GSE or private). Over the last year, approximately 7% of our repurchase demands from GSEs had mortgage insurance rescission as one of the reasons for the

repurchase demand. Of all the mortgage insurance rescission notices received in 2012, approximately 78% have resulted in repurchase demands through December 2013.

Not all mortgage insurance rescissions received in 2012 have been completed through the appeals process with the mortgage insurer and, upon successful appeal, we work

with the investor to rescind the repurchase demand.

(3) While the original loan balances related to these demands are presented above, the establishment of the repurchase liability is based on a combination of factors, such as

our appeals success rates, reimbursement by correspondent and other third party originators, and projected loss severity, which is driven by the difference between the

current loan balance and the estimated collateral value less costs to sell the property.

79