Wells Fargo 2013 Annual Report Download - page 218

Download and view the complete annual report

Please find page 218 of the 2013 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

226 -

227

227 -

228

228 -

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

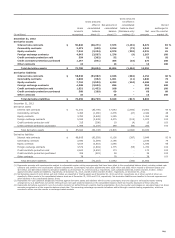

|

|

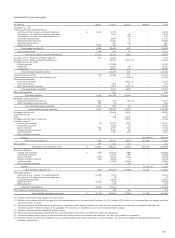

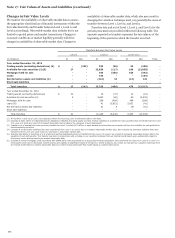

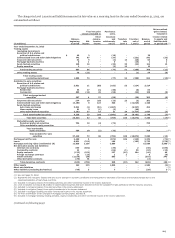

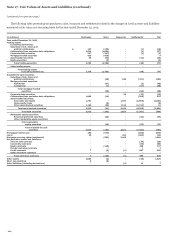

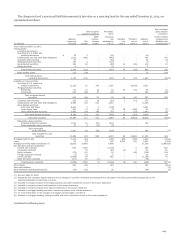

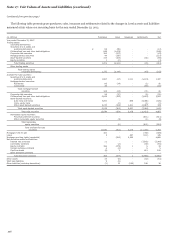

Note 17: Fair Values of Assets and Liabilities (continued)

techniques, such as weighting of internal models and vendor or

broker pricing, where the unobservable inputs are significant to

the overall fair value measurement. Securities classified as Level

3 include certain residential and commercial MBS, other asset-

backed securities, CDOs and certain CLOs, and certain residual

and retained interests in residential mortgage loan

securitizations. We value CDOs using the prices of similar

instruments, the pricing of completed or pending third party

transactions or the pricing of the underlying collateral within the

CDO. Where vendor or broker prices are not readily available,

we use management's best estimate.

MORTGAGES HELD FOR SALE (MHFS) We carry substantially

all of our residential MHFS portfolio at fair value. Fair value is

based on quoted market prices, where available, or the prices for

other mortgage whole loans with similar characteristics. As

necessary, these prices are adjusted for typical securitization

activities, including servicing value, portfolio composition,

market conditions and liquidity. Most of our MHFS are classified

as Level 2. For the portion where market pricing data is not

available, we use a discounted cash flow model to estimate fair

value and, accordingly, classify as Level 3.

LOANS HELD FOR SALE (LHFS) LHFS are carried at the lower

of cost or market value, or at fair value. The fair value of LHFS is

based on what secondary markets are currently offering for loans

with similar characteristics. As such, we classify those loans

subjected to nonrecurring fair value adjustments as Level 2.

LOANS For information on how we report the carrying value of

loans, including PCI loans, see Note 1. Although most loans are

not recorded at fair value on a recurring basis, reverse mortgages

are recorded at fair value on a recurring basis. In addition, we

record nonrecurring fair value adjustments to loans to reflect

partial write-downs that are based on the observable market

price of the loan or current appraised value of the collateral.

We provide fair value estimates in this disclosure for loans

that are not recorded at fair value on a recurring or nonrecurring

basis. Those estimates differentiate loans based on their

financial characteristics, such as product classification, loan

category, pricing features and remaining maturity. Prepayment

and credit loss estimates are evaluated by product and loan rate.

The fair value of commercial loans is calculated by

discounting contractual cash flows, adjusted for credit loss

estimates, using discount rates that are appropriate for loans

with similar characteristics and remaining maturity.

For real estate 1-4 family first and junior lien mortgages, we

calculate fair value by discounting contractual cash flows,

adjusted for prepayment and credit loss estimates, using

discount rates based on current industry pricing (where readily

available) or our own estimate of an appropriate discount rate

for loans of similar size, type, remaining maturity and repricing

characteristics.

The carrying value of credit card loans, which is adjusted for

estimates of credit losses inherent in the portfolio at the balance

sheet date, is reported as a reasonable estimate of fair value. For

all other consumer loans, the fair value is generally calculated by

discounting the contractual cash flows, adjusted for prepayment

and credit loss estimates, based on the current rates we offer for

loans with similar characteristics.

Loan commitments, standby letters of credit and commercial

and similar letters of credit generate ongoing fees at our current

pricing levels, which are recognized over the term of the

commitment period. In situations where the credit quality of the

counterparty to a commitment has declined, we record an

allowance. A reasonable estimate of the fair value of these

instruments is the carrying value of deferred fees plus the related

allowance. Certain letters of credit that are hedged with

derivative instruments are carried at fair value in trading assets

or liabilities. For those letters of credit, fair value is calculated

based on readily quotable credit default spreads using a market

risk credit default swap model.

DERIVATIVES Quoted market prices are available and used for

our exchange-traded derivatives, such as certain interest rate

futures and option contracts, which we classify as Level 1.

However, substantially all of our derivatives are traded in over-

the-counter (OTC) markets where quoted market prices are not

always readily available. Therefore we value most OTC

derivatives using internal valuation techniques. Valuation

techniques and inputs to internally-developed models depend on

the type of derivative and nature of the underlying rate, price or

index upon which the derivative's value is based. Key inputs can

include yield curves, credit curves, foreign-exchange rates,

prepayment rates, volatility measurements and correlation of

such inputs. Where model inputs can be observed in a liquid

market and the model does not require significant judgment,

such derivatives are typically classified as Level 2 of the fair

value hierarchy. Examples of derivatives classified as Level 2

include generic interest rate swaps, foreign currency swaps,

commodity swaps, and certain option and forward contracts.

When instruments are traded in less liquid markets and

significant inputs are unobservable, such derivatives are

classified as Level 3. Examples of derivatives classified as Level 3

include complex and highly structured derivatives, certain credit

default swaps, interest rate lock commitments written for our

residential mortgage loans that we intend to sell and long dated

equity options where volatility is not observable. Additionally,

significant judgments are required when classifying financial

instruments within the fair value hierarchy, particularly between

Level 2 and 3, as is the case for certain derivatives.

MORTGAGE SERVICING RIGHTS (MSRs) AND CERTAIN

OTHER INTERESTS HELD IN SECURITIZATIONS MSRs and

certain other interests held in securitizations (e.g., interest-only

strips) do not trade in an active market with readily observable

prices. Accordingly, we determine the fair value of MSRs using a

valuation model that calculates the present value of estimated

future net servicing income cash flows. The model incorporates

assumptions that market participants use in estimating future

net servicing income cash flows, including estimates of

prepayment speeds (including housing price volatility), discount

rates, default rates, cost to service (including delinquency and

foreclosure costs), escrow account earnings, contractual

servicing fee income, ancillary income and late fees. Commercial

MSRs are carried at lower of cost or market value, and therefore

216