Wells Fargo 2013 Annual Report Download - page 164

Download and view the complete annual report

Please find page 164 of the 2013 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

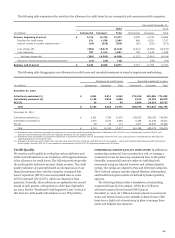

Note 5: Investment Securities (continued)

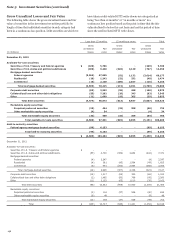

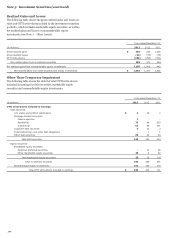

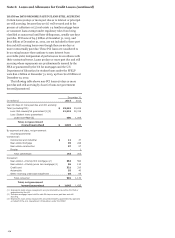

To determine credit impairment losses for asset-backed

securities (e.g., residential MBS, commercial MBS), we estimate

expected future cash flows of the security by estimating the

expected future cash flows of the underlying collateral and

applying those collateral cash flows, together with any credit

enhancements such as subordinated interests owned by third

parties, to the security. The expected future cash flows of the

underlying collateral are determined using the remaining

contractual cash flows adjusted for future expected credit losses

(which consider current delinquencies and nonperforming assets

(NPAs), future expected default rates and collateral value by

vintage and geographic region) and prepayments. The expected

cash flows of the security are then discounted at the security’s

current effective interest rate to arrive at a present value

amount. Total credit impairment losses on residential MBS that

we do not intend to sell are shown in the table below. The table

also presents a summary of the significant inputs considered in

determining the measurement of the credit loss component

recognized in earnings for residential MBS.

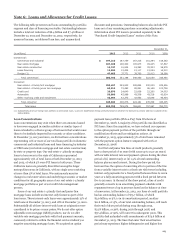

Year ended December 31,

($ in millions) 2013 2012 2011

Credit impairment losses on residential MBS

Investment grade $ - -5

Non-investment grade 72 84 247

Total credit impairment losses on residential MBS $ 72 84 252

Significant inputs (non-agency – non-investment grade MBS)

Expected remaining life of loan loss rate (1):

Range (2) 0-20 % 1-44 0-48

Credit impairment loss rate distribution (3):

0 - 10% range 91 77 42

10 - 20% range 8 11 18

20 - 30% range 1 4 28

Greater than 30% - 8 12

Weighted average loss rate (4) 6 8 12

Current subordination levels (5):

Range (2) 0-41 0-57 0-25

Weighted average (4) -2 4

Prepayment speed (annual CPR (6)):

Range (2) 4-27 5-29 3-19

Weighted average (4) 16 15 11

(1) Represents future expected credit losses on each pool of loans underlying respective securities expressed as a percentage of the total current outstanding loan balance of the

pool for each respective security.

(2) Represents the range of inputs/assumptions based upon the individual securities within each category.

(3) Represents distribution of credit impairment losses recognized in earnings categorized based on range of expected remaining life of loan losses. For example 91% of credit

impairment losses recognized in earnings for the year ended December 31, 2013, had expected remaining life of loan loss assumptions of 0 to 10%.

(4) Calculated by weighting the relevant input/assumption for each individual security by current outstanding amortized cost basis of the security.

(5) Represents current level of credit protection provided by tranches subordinate to our security holdings (subordination), expressed as a percentage of total current underlying

loan balance.

(6) Constant prepayment rate.

Total credit impairment losses on commercial MBS that we

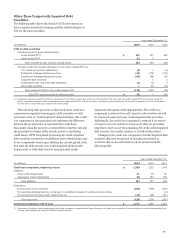

do not intend to sell were $28 million, $86 million, and

$101 million for the years ended December 31, 2013, 2012 and

2011, respectively. Significant inputs considered in determining

the credit impairment losses for commercial MBS are the

expected remaining life of loan loss rates and current

subordination levels. Prepayment activity on commercial MBS

does not significantly impact the determination of their credit

impairment because, unlike residential MBS, commercial MBS

experience significantly lower prepayments due to certain

contractual restrictions, impacting the borrower’s ability to

prepay the mortgage. The expected remaining life of loan loss

rates for commercial MBS with credit impairment losses ranged

from 4% to 15%, 3% to 18%, and 4% to 18%, while the current

subordination level ranges were 0% to 21%, 0% to 13%, and 3%

to 15% for the years ended December 31, 2013, 2012 and 2011,

respectively.

162