Wells Fargo 2013 Annual Report Download - page 56

Download and view the complete annual report

Please find page 56 of the 2013 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

|

|

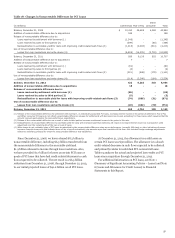

Risk Management – Credit Risk Management (continued)

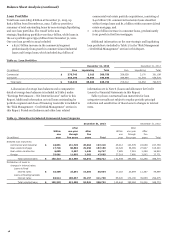

Credit Risk Management

Loans represent the largest component of assets on our balance

sheet and their related credit risk is a significant risk we

manage. We define credit risk as the risk of loss associated with

a borrower or counterparty default (failure to meet obligations

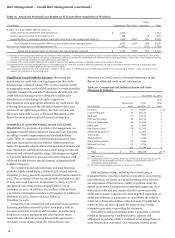

in accordance with agreed upon terms). Table 16 presents our

total loans outstanding by portfolio segment and class of

financing receivable.

Table 16: Total Loans Outstanding by Portfolio Segment and

Class of Financing Receivable

December 31,

(in millions) 2013 2012

Commercial:

Commercial and industrial $ 197,210 187,759

Real estate mortgage 107,100 106,340

Real estate construction 16,747 16,904

Lease financing 12,034 12,424

Foreign (1) 47,665 37,771

Total commercial 380,756 361,198

Consumer:

Real estate 1-4 family first mortgage 258,497 249,900

Real estate 1-4 family junior lien mortgage 65,914 75,465

Credit card 26,870 24,640

Automobile 50,808 45,998

Other revolving credit and installment 42,954 42,373

Total consumer 445,043 438,376

Total loans $ 825,799 799,574

(1) Substantially all of our foreign loan portfolio is commercial loans. Loans are

classified as foreign primarily based on whether the borrower’s primary address is

outside of the United States.

We manage our credit risk by establishing what we believe

are sound credit policies for underwriting new business, while

monitoring and reviewing the performance of our existing loan

portfolios. We employ various credit risk management and

monitoring activities to mitigate risks associated with multiple

risk factors affecting loans we hold, could acquire or originate

including:

x Loan concentrations and related credit quality

x Counterparty credit risk

x Economic and market conditions

x Legislative or regulatory mandates

x Changes in interest rates

x Merger and acquisition activities

x Reputation risk

Our credit risk management oversight process is governed

centrally, but provides for decentralized management and

accountability by our lines of business. Our overall credit

process includes comprehensive credit policies, disciplined

credit underwriting, frequent and detailed risk measurement

and modeling, extensive credit training programs, and a

continual loan review and audit process.

A key to our credit risk management is adherence to a well-

controlled underwriting process, which we believe is

appropriate for the needs of our customers as well as investors

who purchase the loans or securities collateralized by the loans.

54