Singapore Airlines 2002 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2002 Singapore Airlines annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

66

Notes to the Financial Statements

31 March 2002

SIA Annual Report 01/02

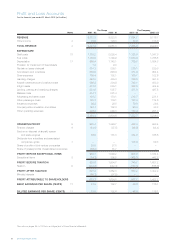

2 Accounting Policies (continued)

Change in accounting estimate

The useful life and residual value of new passenger aircraft, spares and spare engines have been extended from 10 years and

20% to 15 years and 10% on 1 April 2001. The revised depreciation rates are applied prospectively without adjustments to

previously reported amounts. This change has reduced current year depreciation charges of the Group and the Company by

approximately $274.5 million and $265.0 million respectively.

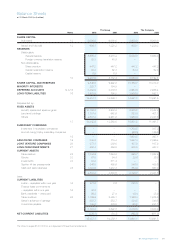

(b) Consolidation

The consolidated financial statements incorporate the financial statements of the Company and all its subsidiary companies for

the financial year ended 31 March. A list of the Group’s subsidiary companies is shown in note 18 to the financial statements.

(c) Subsidiary, joint venture and associated companies

Shares in subsidiary, joint venture and associated companies are stated at cost, less provision for impairment in value.

An associated company is defined as a company, not being a subsidiary company or joint venture company, in which the Group

has a long-term interest of not less than 20% in the equity and in whose financial and operating policy decisions the Group

exercises significant influence.

The Group’s share of the results of associated companies is included in the consolidated profit and loss account and the Group’s

share of the post-acquisition reserves is added to the value of investments in associated companies shown in the consolidated

balance sheet. Except for Air NZ, these amounts are taken from the last audited financial statements of the companies

concerned, made up as appropriate, to the end of the financial year.

The consolidated financial statements incorporate the Group’s share of Air NZ’s results for the period 1 January to 31 December

2001. With the announcement by Air NZ of the completion of its recapitalization package on 18 January 2002, SIA’s equity

interest in Air NZ was diluted to 6.47%. As such, SIA no longer equity accounts for its share of Air NZ’s results effective January

2002. A list of the Group’s associated companies is shown in note 19 to the financial statements.

A joint venture company is defined as a company, not being a subsidiary company, in which the Group has a long–term interest

of not more than 50% in the equity and has joint control of the company’s commercial and financial affairs.

The Group’s share of the consolidated results of the joint venture companies and their subsidiary companies are included in the

consolidated financial statements under the equity method on the same basis as associated companies. A list of the Group’s joint

venture companies is shown in note 20 to the financial statements.

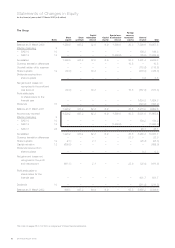

(d) Goodwill

When subsidiary companies or interests in joint venture and associated companies are acquired, any excess of the consideration

over the fair value of the net assets as at the date of acquisition represents goodwill. Goodwill arising from business combinations

on or after 1 April 2001 is amortized using the straight-line method over a period not exceeding twenty years.

Goodwill arising from business combinations prior to that date has been written-off against Group reserves in the financial year in

which it arose. When determining goodwill, assets and liabilities of the acquired interest are translated using the exchange rate at

the date of acquisition if the financial statements of the acquired interest are not denominated in Singapore dollars.

(e) Foreign currencies

Foreign currency transactions are converted into Singapore dollars at exchange rates which approximate bank rates prevailing at

dates of transactions, after taking into account the effect of forward currency contracts which expired during the financial year.

All foreign currency monetary assets and liabilities are translated into Singapore dollars using year-end exchange rates. Non-

monetary assets and liabilities are translated using exchange rates that existed when the values were determined. Gains and

losses arising from conversion of current assets and liabilities are dealt with in the profit and loss account.

For the purposes of the group financial statements, the net assets and the results of the foreign subsidiary companies,

associated companies and joint venture companies are translated into Singapore dollars at the exchange rates ruling at the

balance sheet date. The resulting gains or losses on exchange are taken to foreign currency translation reserve.