Entergy 2004 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2004 Entergy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92

|

|

-80 -

Entergy Corporation and Subsidiaries 2004

NOTES to CONSOLIDATED FINANCIAL STATEMENTS continued

Entergy’s trust asset investment strategy is to invest the assets in

amanner whereby long-term earnings on the assets (plus cash

contributions) provide adequate funding for retiree benefit

payments. The mix of assets is based on an optimization study that

identifies asset allocation targets in order to achieve the maximum

return for an acceptable level of risk, while minimizing the

expected contributions and pension and postretirement expense.

In the optimization study, Entergy formulates assumptions (or

hires a consultant to provide such analysis) about characteristics,

such as expected asset class investment returns, volatility (risk), and

correlation coefficients among the various asset classes. The future

market assumptions used in the optimization study are determined

by examining historical market characteristics of the various asset

classes, and making adjustments to reflect future conditions

expected to prevail over the study period.

The optimization analysis utilized in Entergy’s latest study

produced the following approved asset class target allocations.

Pension Postretirement

Domestic EquitySecurities 45% 37%

International Equity Securities 20% 14%

Fixed–Income Securities 31% 49%

Other (Cash and GACs) 4% 0%

These allocation percentages combined with each asset class’

expected investment returnproduced an aggregate return

expectation for the five years following the study of 7.6% for

pension assets, 5.40% for taxable postretirement assets, and 7.2%

for non-taxable postretirement assets. These returns are not

inconsistent with Entergy’s disclosed expected pre-tax return on

assets of 8.50% over the life of the respective liabilities.

Since precise allocation targets are inefficient to manage security

investments, the following ranges were established to produce an

acceptable economically efficient plan to manage to targets:

Pension Postretirement

Domestic Equity Securities 45% to 55% 32% to 42%

International Equity Securities 15% to 25% 9% to 19%

Fixed–Income Securities 25% to 35% 44% to 54%

Other 0% to 10% 0% to 5%

Accumulated Pension Benefit Obligation

The accumulated benefit obligation for Entergy’s pension plans was

$2.3 billion and $2.1 billion at December 31, 2004 and 2003,

respectively.

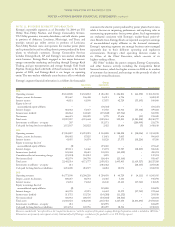

Estimated Future Benefit Payments

Based upon the assumptions used to measure the company’s

pension and postretirement benefit obligation at December 31,

2004, and including pension and postretirement benefits

attributable to estimated future employee service, Entergy expects

that benefits to be paid over the next ten years will be as follows

(in thousands):

Estimated Future Benefits Payments

Years Pension Postretirement

2005 $115,203 $ 60,932

2006 $116,894 $ 59,761

2007 $119,092 $ 62,392

2008 $122,728 $ 64,381

2009 $127,877 $ 66,444

2010 – 2014 $780,295 $360,191

Contributions

Entergy expects to contribute $185.9 million (excluding about

$1.2 million in employee contributions) to its pension plans and

$63.3 million to other postretirement plans in 2005.

Additional Information

The change in the minimum pension liability included in other

comprehensive income and regulatory assets was as follows for 2004

and 2003 (in thousands):

2004 2003

Increase/(decrease) in the minimum

pension liability included in:

Other comprehensive income $(4,578) $ (1,639)

Regulatory assets $73,311 $(23,768)

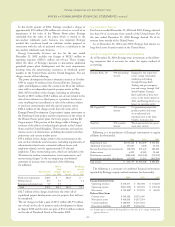

Actuarial Assumptions

The assumed health care cost trend rate used in measuring the

APBO of Entergywas 10% for 2005, gradually decreasing each

successive year until it reaches 4.5% in 2011 and beyond. The

assumed health care cost trend rate used in measuring the Net

Other Postretirement Benefit Cost of Entergy was 10% for 2004,

graduallydecreasing eachsuccessive year until it reaches 4.5% in

2010 and beyond. A one percentage point change in the assumed

health carecost trend rate for 2004 would havethe following effects

(in thousands):

1Percentage Point Increase 1 Percentage Point Decrease

Impact Impact

on the sum of on the sum of

Impact on service costs and Impact on service costs and

2004 the APBO interest cost the APBO interest cost

Entergy

Corporation $99,271 $11,587 $(89,801) $(10,061)

The significant actuarial assumptions used in determining the

pension PBO and the SFAS 106 APBO for 2004, 2003, and 2002

were as follows:

2004 2003 2002

Weighted-average discount rate:

Pension 6.00% 6.25% 6.75%

Other postretirement 6.00% 6.71% 6.75%

Weighted-average rate of increase

in future compensation levels 3.25% 3.25% 3.25%

Expected long-term rate of

return on plan assets:

Taxable assets 5.50% 5.50% 5.50%

Non-taxable assets 8.50% 8.75% 8.75%