Entergy 2004 Annual Report Download - page 30

Download and view the complete annual report

Please find page 30 of the 2004 Entergy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

-28 -

Entergy Corporation and Subsidiaries 2004

LIQUIDITY AND CAPITAL RESOURCES

This section discusses Entergy’s capital structure, capital spending

plans and other uses of capital, sources of capital, and the cash flow

activity presented in the cash flow statement.

Capital Structure

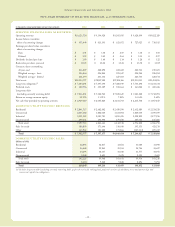

Entergy’s capitalization is balanced between equity and debt, as

shown in the following table. The reduction in the debt to capital

percentage from 2002 to 2003 is the result of reduced debt

outstanding in the U.S. Utility and Non-Utility Nuclear businesses,

and an increase in shareholders’ equity, primarily due to increased

retained earnings.

2004 2003 2002

Net debt to net capital at the end of the year 44.7% 45.3% 47.7%

Effect of subtracting cash from debt 2.7% 2.2% 4.1%

Debt to capital at the end of the year 47.4% 47.5% 51.8%

Net debt consists of debt less cash and cash equivalents. Debt

consists of notes payable, capital lease obligations, preferred stock

with sinking fund, and long-term debt, including the currently

maturing portion. Capital consists of debt, commonshareholders’

equity, and preferred stock without sinking fund. Net capital

consists of capital less cash and cash equivalents. The preferred

stockwith sinking fund is included in debt pursuant to SFAS 150,

which Entergy implemented in the third quarter of 2003. The 2002

ratio does not reflect that type of security as debt, but does include

it in net capital, which is how Entergy presented those securities

prior to implementation of SFAS 150. Entergy uses the net debt to

net capital ratio in analyzing its financial condition and believes it

provides useful informationto its investors and creditors in

evaluating Entergy’s financial condition.

Long-term debt, including the currently maturing portion, makes

up over 90% of Entergy’s total debt outstanding. Following are

Entergy’s long-term debt principal maturities as of December 31,

2003 and 2004 by operating segment. The figures below include

principal payments on the Entergy Louisiana and System Energy

sale-leaseback transactions, which are included in long-term debt

on the balance sheet (in millions):

Long-term 2008- After

Debt Maturities 2004 2005 2006 2007 2009 2009

As of December 31, 2003

U.S. Utility $450 $355 $ 28 $573 $ 721 $4,305

Non-Utility Nuclear 74 72 76 80 40 173

EnergyCommodity

Services – – – – – –

Parent and Other – 60 – – 539 301

Total $524 $487 $104 $653 $1,300 $4,779

As of December 31, 2004

U.S. Utility – $359 $ 27 $ 98 $ 749 $4,880

Non-Utility Nuclear – 77 76 80 40 173

EnergyCommodity

Services – – – – – –

Parent and Other – 60 – 50 539 301

Total – $496 $103 $228 $1,328 $5,354

Note 5 to the consolidated financial statements provides more

detail concerning long-term debt.

In May 2004, Entergy Corporation replaced its 364-day bank

credit facility with two separate facilities, a new 364-day credit

facility and a three-year credit facility. The three-year credit

facility, which expires in May 2007, has a borrowing capacity

of $965 million, of which $50 million was outstanding at

December 31, 2004.

In December 2004, Entergy Corporation refinanced the 364-day

bank credit facility by entering into a five-year credit facility. The

five-year credit facility, which expires in December 2009, has a

borrowing capacity of $500 million, none of which was outstanding

at December 31, 2004.

Entergy also has the ability to issue letters of credit against the

total borrowing capacity of both credit facilities, and $50 million of

letters of credit had been issued against the three-year facility at

December 31, 2004.

EntergyCorporation’s credit facilities require it to maintain a

consolidated debt ratio of 65% or less of its total capitalization, and

maintain an interest coverage ratio of 2 to 1. If Entergy fails to meet

these limits, or if Entergy or the domestic utility companies default

on other indebtedness or are in bankruptcy or insolvency

proceedings, an acceleration of the credit facilities’ maturity

dates may occur.

Capital lease obligations, including nuclear fuel leases, are a

minimal part of Entergy’s overall capital structure, and are discussed

further in Note 9 to the consolidated financial statements.

Following are Entergy’s payment obligations under those leases

(in millions):

2008- After

2005 2006 2007 2009 2009

Capital lease payments,

including nuclear fuel leases $136 $143 $3 $2 $3

Notes payable, which include borrowings outstanding on credit

facilities with original maturities of less than one year, were less than

$1 million as of December 31, 2004. Entergy Arkansas, Entergy

Louisiana, Entergy Mississippi, and Entergy New Orleans each

have 364-day credit facilities available as follows:

Expiration Amount of Amount Drawn as

Company Date Facility of Dec. 31, 2004

Entergy Arkansas April 2005 $85 million –

Entergy Louisiana April 2005 $15 million(a) –

Entergy Mississippi May 2005 $25 million –

Entergy New Orleans April 2005 $14 million(a) –

(a) The combined amount borrowed by Entergy Louisiana and Entergy New Orleans

under these facilities at any one time cannot exceed $15 million.

Operating Lease Obligations and Guarantees

of Unconsolidated Obligations

Entergyhas a minimal amount of operating lease obligations and

guarantees in support of unconsolidated obligations. Entergy’s

guarantees in support of unconsolidated obligations are not likely to

have a material effect onEntergy’s financial condition or results

MANAGEMENT’S FINANCIAL DISCUSSION and ANALYSIS continued