Entergy 2004 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2004 Entergy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

-58 -

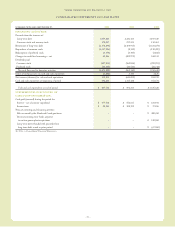

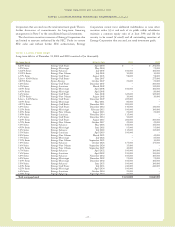

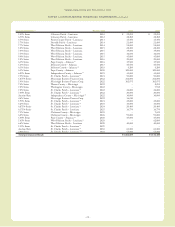

Entergy Corporation and Subsidiaries 2004

Equity Method Investees

Entergy owns investments that are accounted for under the equity

method of accounting because Entergy’s ownership level results in

significant influence, but not control, over the investee and its

operations. Entergy records its share of earnings or losses of the

investee based on the change during the period in the estimated

liquidation value of the investment, assuming that the investee’s

assets were to be liquidated at book value. The equity earnings for

Entergy-Koch, LP recorded by Entergy are dictated by the terms of

the partnership agreement in accordance with the hypothetical

liquidation at book value (HLBV) method. In accordance with the

HLBV method, earnings are allocated to members based on what

each partner would receive from their capital account if,

hypothetically, liquidation were to occur at the balance sheet date

and amounts distributed were based on recorded book values.

Entergy discontinues the recognition of losses on equity

investments when its share of losses equals or exceeds its carrying

amount of investee plus any advances made or commitments to

provide additional financial support. See Note 12 to the

consolidated financial statements for additional information

regarding Entergy’s equity method investments.

Derivative Financial Instruments and

Commodity Derivatives

SFAS 133, “Accounting for Derivative Instruments and Hedging

Activities,” requires that all derivatives be recognized in the balance

sheet, either as assets or liabilities, at fair value, unless theymeet the

normal purchase, normal sales criteria. The changes in the fair value

of recognized derivatives are recorded each period in current

earnings or other comprehensiveincome, depending on whether a

derivativeis designated as partof a hedge transaction and the type

of hedge transaction.

Contracts for commodities that will be delivered in quantities

expected to be used or sold in the ordinarycourse of business,

including certain purchases and sales of power and fuel, are not

classified as derivatives. These contracts are exempted under the

normal purchase, normal sales criteria of SFAS 133. Revenues and

expenses fromthese contracts are reported on a gross basis in the

appropriate revenue and expense categories as the commodities are

received or delivered.

For other contracts for commodities in which Entergy is hedging

the variability of cash flows related to a variable-rate asset, liability,

or forecasted transactions that qualify as cash flow hedges, the

changes in the fair value of suchderivativeinstruments are reported

in other comprehensive income. To qualify for hedge accounting,

the relationship between the hedging instrument and the hedged

item must be documented to include the risk management objective

and strategyand, at inception and on an ongoing basis, the effec-

tiveness of the hedge in offsetting the changes in the cash flows of

the item being hedged. Gains or losses accumulated in other com-

prehensiveincome are reclassified as earnings in the periods in

which earnings are affected by the variability of the cash flows of the

hedged item. The ineffectiveportions of all hedges are recognized

in current-period earnings.

Impairment of Long-Lived Assets

Entergy periodically reviews long-lived assets held in all of its

business segments whenever events or changes in circumstances

indicate that recoverability of these assets is uncertain. Generally,

the determination of recoverability is based on the undiscounted net

cash flows expected to result from such operations and assets.

Projected net cash flows depend on the future operating costs

associated with the assets, the efficiency and availability of the assets

and generating units, and the future market and price for

energy over the remaining life of the assets. See Note 11 to the

consolidated financial statements for a discussion of asset

impairments recognized by Entergy in 2002 and 2004.

River Bend AFUDC

The River Bend AFUDC gross-up is a regulatory asset that

represents the incremental difference imputed by the Louisiana

Public Service Commission (LPSC) between the AFUDC actually

recorded by Entergy Gulf States on a net-of-tax basis during the

construction of River Bend and what the AFUDC would have been

on a pre-tax basis.The imputed amount was only calculated on that

portion of River Bend that the LPSC allowed in rate base and is

being amortized over the estimated remaining economic life of

River Bend.

Transitionto CompetitionLiabilities

In conjunction with electric utility industry restructuring activity in

Texas, regulatory mechanisms were established to mitigate

potential stranded costs. Texas restructuring legislation allowed

depreciation on transmission and distribution assets to be directed

toward generation assets. The liability recorded as a result of this

mechanism is classified as “transitionto competition” deferred

credits on the balance sheet.

Reacquired Debt

The premiums and costs associated with reacquired debt of the

domestic utilitycompanies and System Energy (except that portion

allocable to the deregulated operations of Entergy Gulf States)

arebeing amortized over the life of the related new issuances, in

accordance with ratemaking treatment.

Foreign Currency Translation

All assets and liabilities of Entergy’s foreign subsidiaries are

translated into U.S. dollars at the exchange rate in effect at the end

of the period. Revenues and expenses are translated at average

exchange rates prevailing during the period. The resulting

translation adjustments are reflected in a separate component of

shareholders’ equity. Current exchange rates are used for U.S.

dollar disclosures of future obligations denominated in

foreign currencies.

New Accounting Pronouncements

During 2004, Entergy adopted the provisions of FASB Staff

Position(FSP) 106-2, “Accounting and Disclosure Requirements

Related to Medicare Prescription Drug, Improvement and

Modernization Act of 2003,” which is discussed further in Note 10

to the consolidated financial statements. Entergy also adopted

NOTES to CONSOLIDATED FINANCIAL STATEMENTS continued