Entergy 2004 Annual Report Download - page 34

Download and view the complete annual report

Please find page 34 of the 2004 Entergy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

-32 -

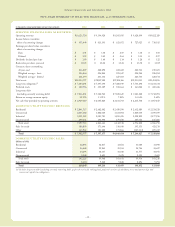

Entergy Corporation and Subsidiaries 2004

•The Non-Utility Nuclear business provided $415 million

in cash from operating activities compared to providing

$183 million in 2003. The increase resulted primarily from

lower intercompany income tax payments and increases in

generation and contract pricing that led to an

increase in revenues.

•Entergy’s investment in Entergy-Koch, LP provided

$526 million in cash from operating activities compared to

using $41 million in 2003. Entergy received dividends from

Entergy-Koch of $529 million in 2004 compared to

$100 million in 2003. In addition, tax payments related to the

investment were higher in 2003 because the investment had

higher net income in 2003.

•The non-nuclear wholesale assets business used $46 million in

cash from operating activities compared to using $70 million

in 2003. The decrease in cash used resulted primarily from a

one-time $33 million payment in 2003 related to a generation

contract in the non-nuclear wholesale assets business.

•The parent company, Entergy Corporation, used $146 million

in cash fromoperating activities in 2004 compared to providing

$209 million in 2003 primarily due to higher intercompany

income tax payments.

As discussed in Note 3 to the consolidated financial statements, in

2003, the domestic utility companies and System Energy filed, with

the Internal Revenue Service (IRS), a change in tax accounting

method notification for their respective calculations of cost of goods

sold. The cash benefit fromthe method change was $74 millionon

a consolidated basis in 2004. This accounting method change is

an issue across the utility industry and will likely be challenged by

the IRS onaudit. As of December 31, 2004, Entergyhas a

consolidated net operating loss (NOL) carryforward for tax

purposes of $2.9 billion, principally resulting from the change in

tax accounting method related to cost of goods sold. If the tax

accounting method change is sustained, Entergy expects to fully

utilize the NOL carryforward through 2006.

2003 Compared to 2002

Entergy’s cash flow provided by operating activities decreased in

2003 primarily due to the following:

•The U.S. Utilityprovided $1,675 million in operating cash flow

in 2003 compared to providing $2,341 million in 2002. The

decrease primarily resulted from the tax accounting election

made by Entergy Louisiana, as discussed below. Also

contributing to the decrease were higher payments for fuel

during the period, whichalso significantly increased the amount

of deferred fuel costs.

•The non-nuclear wholesale assets business used $70 million in

operating cash flowin 2003 compared to providing $43 million

in 2002 primarilydue to a decrease of $64 millionin the

income tax refund received in 2003 compared to 2002. Also

contributing to the increase in cash used was a one-time

$33 millionpayment in 2003 related to a generationcontract in

the non-nuclear wholesale assets business.

•The Non-Utility Nuclear segment provided $183 million in

operating cash flow in 2003 compared to providing

$282 million in 2002 primarily due to higher tax payments and

unplanned outages.

•Operating cash flow used by the investment in Entergy-Koch,

LP decreased by $6 million in 2003. This decrease in cash flow

used was due to the receipt of $100 million in dividends from

Entergy-Koch in 2003. Almost entirely offsetting the dividends

received was an increase in tax payments related to Entergy’s

investment in Entergy-Koch due to increased income from

the investment.

Partially offsetting the decrease in cash flow in 2003 was an increase

due to the parent company providing $209 million in operating cash

flow in 2003 compared to using $439 million in 2002 primarily due

to the payment that Entergy Corporation made to Entergy

Louisiana in 2002 pursuant to the tax accounting election made by

Entergy Louisiana.

In 2001, Entergy Louisiana changed its method of accounting

for tax purposes related to its wholesale electric power contracts.

The most significant of these is the contract to purchase power from

the Vidalia project (the contract is discussed in Note 8 to the

consolidated financial statements). The new tax accounting method

has provided a cumulative cash flow benefit of approximately

$790 million through 2004, which is expected to reverse in the years

2005 through 2031. The election did not reduce book income tax

expense. The timing of the reversal of this benefit depends on

several variables, including the price of power. Approximately half

of the consolidated cash flowbenefit of the election occurred in

2001 and the remainder occurred in 2002. In accordance with

Entergy’s intercompany tax allocation agreement, the cash flow

benefit for Entergy Louisiana occurred in the fourth

quarter of 2002.

In a September 2002 settlement of an LPSC proceeding that

concerned the Vidalia contract, the LPSC approved Entergy

Louisiana’s proposed treatment of the regulatory impact of the tax

accounting election. In general, the settlement permits Entergy

Louisiana to keep a portion of the tax benefit in exchange for

bearing the risk associated with sustaining the tax treatment. The

LPSC settlement divided the term of the Vidalia contract into two

segments: 2002-2012 and 2013-2031. During the first eight years

of the 2002-2012 segment, Entergy Louisiana agreed to credit rates

by flowing through its fuel adjustment calculation $11 million each

year, beginning monthlyin October 2002. Entergy Louisiana must

credit rates in this way and by this amount even if Entergy

Louisiana is unable to sustain the tax deduction. Entergy Louisiana

also must credit rates by $11 millioneach year for an additional

two years unless either the tax accounting method elected is

retroactively repealed or the Internal Revenue Service denies the

entire deduction related to the tax accounting method. Entergy

Louisiana agreed to credit ratepayers additional amounts unless the

tax accounting election is not sustained if it is challenged. During

2013-2031, Entergy Louisiana and its ratepayers would share the

remaining benefits of this tax accounting election.

MANAGEMENT’S FINANCIAL DISCUSSION and ANALYSIS continued