Entergy 2004 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2004 Entergy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

-42 -

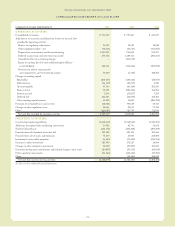

Entergy Corporation and Subsidiaries 2004

States and Entergy’s Non-Utility Nuclear business increased

income by approximately $28.9 million net-of-tax for the excess

of the reduction in the liability over the amount of

undepreciated asset retirement cost at the time of adoption of

SFAS 143. The changes in probability for ANO 1 and ANO 2

had no effect on net income because, as discussed further below,

any amounts recorded related to SFAS 143 are offset by the

recording of regulatory assets or regulatory liabilities when

projected decommissioning costs are collected in rates. Future

revisions to appropriately reflect changes needed to the estimate

of decommissioning costs will affect net income, only to the

extent that the estimate of any reduction in the liability exceeds

the amount of the undepreciated asset retirement cost at the

date of the revision, for unregulated portions of Entergy’s

business. Any increases in the liability recorded due to such

changes are capitalized and depreciated over the asset’s

remaining economic life in accordance with SFAS 143.

•Spent Fuel Disposal -Federal regulations require the U.S.

Department of Energy (DOE) to provide a permanent

repository for the storage of spent nuclear fuel, and legislation

has been passed by Congress to develop this repository at Yucca

Mountain, Nevada. Until this site is available, however, nuclear

plant operators must provide for interim spent fuel storage on

the nuclear plant site, which can require the construction and

maintenance of dry cask storage sites or other facilities. The

costs of developing and maintaining these facilities can have a

significant effect (as much as 16% of estimated decommission-

ing costs). Entergy’sdecommissioning studies include cost esti-

mates for spent fuel storage. However, these estimates could

change in the future based on the timing of the opening of the

YuccaMountain facility, the schedule for shipments to that

facilitywhen it is opened, or other factors.

•Technology and Regulation - To date, there is limited practical

experience in the United States with actual decommissioning of

large nuclear facilities. As experience is gained and technology

changes, cost estimates could also change. If regulations

regarding nuclear decommissioning were to change, this could

have a potentially significant effect on cost estimates. The effect

of these potential changes is not presently determinable.

Entergy’sdecommissioning cost studies assume current

technologies and regulations.

SFAS 143

Entergy implemented SFAS 143, “Accounting for Asset

Retirement Obligations,” effective January 1, 2003. Nuclear

decommissioning costs comprise substantially all of Entergy’s asset

retirement obligations, and the measurement and recording of

Entergy’s decommissioning obligations changed significantly with

the implementationof SFAS 143. The most significant differences

in the measurement of these obligations are outlined below:

•Recording of full obligation - SFAS 143 requires that the fair

value of an asset retirement obligation be recorded when it is

incurred. This caused the recorded decommissioning obligation

in Entergy’s U.S. Utility business to increase significantly, as

Entergyhad previouslyonly recorded this obligation as the

related costs were collected from customers, and as earnings

were recorded on the related trust funds.

•Fair value approach - SFAS 143 requires that these obligations

be measured using a fair value approach. Among other things,

this entails the assumption that the costs will be incurred by a

third party and will therefore include appropriate profit margins

and risk premiums. Entergy’s decommissioning studies had

been based on Entergy performing the work, and did not

include any such margins or premiums.

•Discount rate - SFAS 143 requires that these obligations be

discounted using a credit-adjusted, risk-free rate.

The net effect on Entergy’s financial statements of implementing

SFAS 143 for the U.S. Utility and Non-Utility Nuclear

businesses follows:

•For the U.S. Utility business, the implementation of SFAS 143

for the rate-regulated business of the domestic utility companies

and System Energy was recorded as regulatory assets, with no

resulting effect on Entergy’s net income. Entergy recorded these

regulatory assets because existing rate mechanisms in each

jurisdiction are based on the original or historical cost standard

that allows Entergy to recover all ultimate costs of

decommissioning existing assets from current and future

customers. As a result of this treatment, SFAS 143 is expected

to be earnings neutral to the rate-regulated business of the

domestic utilitycompanies and System Energy. Upon

implementation of SFAS 143 in 2003, assets and liabilities

increased by $1.1 billion for the U.S. Utility segment as a result

of recording the asset retirement obligations at their fair values

of $1.1 billionas determined under SFAS 143, increasing

utility plant by $288 million, reducing accumulated depreciation

by $361 million and recording the related regulatory assets of

$422 million. The implementation of SFAS 143 for the portion

of River Bend not subject to cost-based ratemaking decreased

earnings by $21 million net-of-tax ($0.09 per share) as a result

of a one-time cumulative effect of accounting change. In

accordance with ratemaking treatment and as required by

SFAS 71, the depreciationprovisions for Entergy’s utility

subsidiaries include a component for removal costs that are not

asset retirement obligations under SFAS 143. Approximately

6% of the U.S. Utility’s current depreciation rates, on a

weighted-average basis, represents a component for the net of

salvage value and removal costs.

•For the Non-Utility Nuclear business, the implementation of

SFAS 143 in 2003 resulted in a decrease in liabilities of

$595 million due to reductions in decommissioning liabilities,

adecrease in assets of $340 million, including a decrease in

electric plant in service of $315 million, and an increase in

earnings of $155 million net-of-tax as a result of the one-time

cumulative effect of accounting change.

Also, beginning in 2003, Entergy’s earnings for the Non-Utility

Nuclear business have an increase of $18 million after-tax because

of the change in accretion of the liability and depreciation of the

adjusted plant costs fromthe 2002 levels. This effect will gradually

decrease over future years as the accretion of the liability increases.

Management expects that applying SFAS 143 post-implementation

will have a minimal effect on ongoing earnings for the

U.S. Utility business.

MANAGEMENT’S FINANCIAL DISCUSSION and ANALYSIS continued