Albertsons 2014 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2014 Albertsons annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

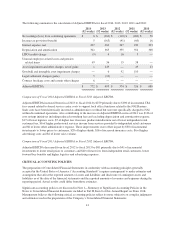

|

|

sale of common stock to Symphony Investors LLC (which is owned by a Cerberus-led investor consortium) in

connection with the NAI Banner Sale in fiscal 2014, $0 of dividend payments in fiscal 2014 compared to $37 of

dividend payments made in fiscal 2013 and $7 of proceeds from the exercise of stock options, offset in part by

$85 of additional cash payments for debt financing and issuance costs associated with the NAI Banner Sale, the

re-pricing of the interest rate on the Secured Term Loan due March 2019 and the refinancing of $372 of the 2016

Senior Notes (defined below). The increase in borrowings compared to last year reflects the usage of cash for

working capital changes as a result of the NAI Banner Sale and an increase in cash used for financing costs and

income taxes.

The increase in cash used in financing activities in fiscal 2013 compared to fiscal 2012 is primarily attributable to

$58 of additional cash payments for debt financing costs, primarily offset by a decrease in cash used for dividend

payments of $37.

Net cash used in the financing activities of discontinued operations were $36, $46 and $94 for fiscal 2014, 2013

and 2012, respectively. The decrease in cash used in discontinued operations’ financing activities in fiscal 2014

compared to last year and from fiscal 2013 to fiscal 2012 is attributable to lower payments on capital lease and

long-term debt obligations.

Annual cash dividends declared for fiscal 2013 and 2012 were $.0875 and $0.3500 per share, respectively.

During fiscal 2013, the Company announced that it had suspended the payment of the regular quarterly dividend.

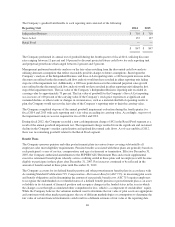

Debt Management and Credit Agreements

The Company’s credit facilities and certain long-term debt agreements have restrictive covenants and cross-

default provisions which generally provide, subject to the Company’s right to cure, for the acceleration of

payments due in the event of a breach of a covenant or a default in the payment of a specified amount of

indebtedness due under certain other debt agreements. The Company was in compliance with all such covenants

and provisions for all periods presented.

Senior Secured Credit Agreements

As of February 23, 2013, there were borrowings outstanding under the Company’s six-year $850 term loan due

August 2018 (the “Secured Term Loan Facility due August 2018”) of $834 at the rate of LIBOR plus 6.75

percent and including a LIBOR floor of 1.25 percent, of which $9 was classified as current. The Secured Term

Loan Facility due August 2018 was also guaranteed by the Company’s material subsidiaries. To secure their

obligations under the Secured Term Loan Facility due August 2018, the Company and the guarantors granted a

perfected first-priority mortgage lien and security interest for the benefit of the facility lenders in certain of their

owned or ground-leased real estate and the equipment located on such real estate. As of February 23, 2013, there

was $302 of owned or ground-leased real estate and associated equipment pledged as collateral, classified as

Property, plant and equipment, net as well as $767 of assets included in Long-term assets of discontinued

operations in the Consolidated Balance Sheets. In addition, the obligations under the Secured Term Loan Facility

due August 2018 were secured by second-priority secured interests in the collateral securing the five-year $1,650

asset-based revolving credit facility (the “Revolving ABL Credit Facility due August 2017”), subject to certain

limitations to ensure compliance with the Company’s outstanding debt instruments and leases.

On March 21, 2013, the Company entered into (i) an amended and restated five-year $1,000 (subject to

borrowing base availability) asset-based revolving credit facility, which pursuant to an accordion feature may be

increased to $1,250 upon our request and subject to the agreement of the lenders participating in the increase (the

“Revolving ABL Credit Facility due March 2018”), secured by the Company’s inventory, credit card receivables

and certain other assets, which bears interest at the rate of LIBOR plus 1.75 percent to LIBOR plus 2.25 percent

or prime plus 0.75 percent to 1.25 percent, with facility fees ranging from 0.25 percent to 0.375 percent,

depending on utilization and (ii) a new six-year $1,500 term loan (the “Secured Term Loan Facility due March

2019”), secured by substantially all of the Company’s real estate, equipment and certain other assets, which bears

51