Xcel Energy 2004 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2004 Xcel Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

|

|

MANAGEMENT’S DISCUSSION and ANALYSIS

Xcel Energy Annual Report 2004

31

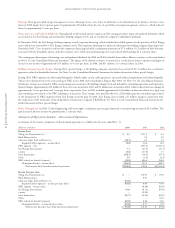

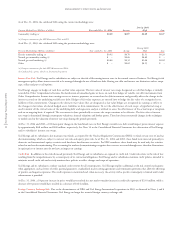

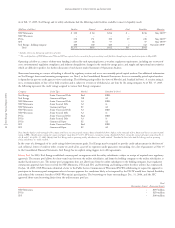

As of Dec. 31, 2004, the sources of fair value of the commodity trading and hedging net assets were as follows:

Commodity Trading Contracts

Futures/Forwards

Source of Maturity Less Maturity Maturity Maturity Greater Total Futures/

(Thousands of dollars) Fair Value than 1 Year 1 to 3 Years 4 to 5 Years than 5 Years Forwards Fair Value

NSP-Minnesota 1$ 51 $ – $ – $ – $ 51

2874 – – – 874

PSCo 1(922) – – – (922)

2(134) – – – (134)

Total futures/forwards fair value $ (131) $ – $ – $ – $ (131)

Options

Source of Maturity Less Maturity Maturity Maturity Greater Total Options

(Thousands of dollars) Fair Value than 1 Year 1 to 3 Years 4 to 5 Years than 5 Years Fair Value

PSCo 2$ 139 $ – $ – $ – $ 139

Total options fair value $ 139 $ – $ – $ – $ 139

Hedge Contracts

Futures/Forwards

Source of Maturity Less Maturity Maturity Maturity Greater Total Futures/

(Thousands of dollars) Fair Value than 1 Year 1 to 3 Years 4 to 5 Years than 5 Years Forwards Fair Value

PSCo 2$ 1,047 $ – $ – $ – $ 1,047

Total futures/forwards fair value $ 1,047 $ – $ – $ – $ 1,047

Options

Source of Maturity Less Maturity Maturity Maturity Greater Total Options

(Thousands of dollars) Fair Value than 1 Year 1 to 3 Years 4 to 5 Years than 5 Years Fair Value

NSP-Minnesota 2$ (7,153) $ – $ – $ – $ (7,153)

NSP-Wisconsin 2(1,060) – – – (1,060)

PSCo 2(18,453) 1,028 – – (17,425)

Total options fair value $(26,666) $1,028 $ – $ – $(25,638)

1 Prices actively quoted or based on actively quoted prices.

2 Prices based on models and other valuation methods. These represent the fair value of positions calculated using internal models when directly and indirectly quoted external prices

or prices derived from external sources are not available. Internal models incorporate the use of options pricing and estimates of the present value of cash flows based upon underlying

contractual terms. The models reflect management’s estimates, taking into account observable market prices, estimated market prices in the absence of quoted market prices, the

risk-free market discount rate, volatility factors, estimated correlations of commodity prices and contractual volumes. Market price uncertainty and other risks also are factored into

the model.

Normal purchases and sales transactions, as defined by SFAS No. 133, as amended, have been excluded.

At Dec. 31, 2004, a 10-percent increase in market prices over the next 12 months for trading contracts would impact pretax income from continuing

operations by approximately $(0.1) million, whereas a 10-percent decrease would impact pretax income from continuing operations by approximately

$0.1 million. Hedge contracts are accounted for as a component of Other Comprehensive Income and would not directly impact earnings.

Xcel Energy’s short-term wholesale and commodity trading operations measure the outstanding risk exposure to price changes on transactions, contracts

and obligations that have been entered into, but not closed, using an industry standard methodology known as Value-at-Risk (VaR). VaR expresses the

potential change in fair value on the outstanding transactions, contracts and obligations over a particular period of time, with a given confidence interval

under normal market conditions. Xcel Energy utilizes the variance/covariance approach in calculating VaR. The VaR model employs a 95-percent confidence

interval level based on historical price movement, lognormal price distribution assumption, delta half-gamma approach for non-linear instruments and

a three-day holding period for both electricity and natural gas. Previously, Xcel Energy calculated VaR using a holding period of five days for electricity

and two days for natural gas. However, the methodology was changed to ensure consistency in risk measurement across both commodities. Xcel Energy’s

revised holding periods remain consistent with current industry practice. VaR using the current methodology for 2004 and previous methodology for

2003 are as follows: