Western Union 2010 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2010 Western Union annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

Unrealized gains and losses on available-for-sale securities are excluded from earnings and presented as a

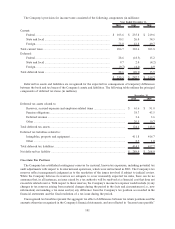

component of accumulated other comprehensive income or loss, net of related deferred taxes. Proceeds from the

sale and maturity of available-for-sale securities during the years ended December 31, 2010, 2009 and 2008 were

$14.7 billion, $8.4 billion and $2.8 billion, respectively. The transition of the money order business from IPS in

October 2009, as described above, increased the frequency of purchases and proceeds received by the Company in

2010.

Gains and losses on investments are calculated using the specific-identification method and are recognized

during the period in which the investment is sold or when an investment experiences an other-than-temporary

decline in value. Factors that could indicate an impairment exists include, but are not limited to: earnings

performance, changes in credit rating or adverse changes in the regulatory or economic environment of the

asset. If potential impairment exists, the Company assesses whether it has the intent to sell the debt security, more

likely than not will be required to sell the debt security before its anticipated recovery or expects that some of the

contractual cash flows will not be received. The Company had no material other-than-temporary impairments

during the periods presented.

The components of investment securities are as follows (in millions):

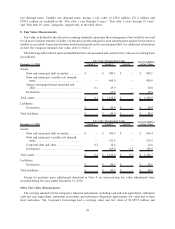

December 31, 2010

Amortized

Cost

Fair

Value

Gross

Unrealized

Gains

Gross

Unrealized

Losses

Net

Unrealized

Gains/(Losses)

State and municipal debt securities (a) ............ $ 844.1 $ 849.1 $ 7.0 $ (2.0) $ 5.0

State and municipal variable rate demand

notes ......................................................... 490.0 490.0 — — —

Agency mortgage-backed securities and

other ......................................................... 29.9 30.0 0.1 — 0.1

$ 1,364.0 $ 1,369.1 $ 7.1 $ (2.0) $ 5.1

December 31, 2009

Amortized

Cost

Fair

Value

Gross

Unrealized

Gains

Gross

Unrealized

Losses

Net

Unrealized

Gains/(Losses)

State and municipal debt securities (a) ............ $ 686.4 $ 696.4 $ 10.6 $ (0.6) $ 10.0

State and municipal variable rate demand

notes ......................................................... 513.8 513.8 — — —

Corporate debt and other ............................... 12.3 12.6 0.3 — 0.3

$ 1,212.5 $ 1,222.8 $ 10.9 $ (0.6) $ 10.3

(a) The majority of these securities are fixed rate instruments.

There were no investments with a single issuer or individual securities representing greater than 10% of total

investment securities as of December 31, 2010 and 2009.

The following summarizes contractual maturities of investment securities as of December 31, 2010 (in millions):

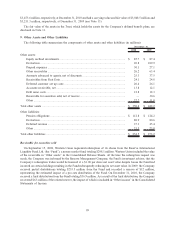

Amortized

Cost

Fair

Value

Due within 1 year ............................................................................................... $ 114.7 $ 115.0

Due after 1 year through 5 years ......................................................................... 659.7 664.4

Due after 5 years through 10 years ...................................................................... 156.0 155.9

Due after 10 years .............................................................................................. 433.6 433.8

$ 1,364.0 $ 1,369.1

Actual maturities may differ from contractual maturities because issuers may have the right to call or prepay the

obligations or the Company may have the right to put the obligation prior to its contractual maturity, as with variable

97