Western Union 2010 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2010 Western Union annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

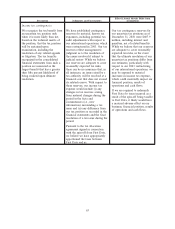

Description Judgments and Uncertainties

Effect if Actual Results Differ from

Assumptions

Acquisitions—Purchase Price

Allocation

We allocate the purchase price of

an acquired business to its

identifiable assets and liabilities

based on estimated fair values.

The excess of the purchase price

over the amount allocated to the

assets and liabilities is recorded as

goodwill.

For most acquisitions, we engage

outside appraisal firms to assist in

the fair value determination of

identifiable intangible assets such

as agent networks, customer

relationships, tradenames and any

other significant assets or

liabilities. We adjust the

preliminary purchase price

allocation, as necessary, after the

acquisition closing date through

the end of the measurement period

of one year or less as we finalize

valuations for the assets acquired

and liabilities assumed.

Purchase price allocation requires

management to make assumptions

and apply judgment to estimate

the fair value of acquired assets

and liabilities. Management

estimates the fair value of assets

and liabilities primarily using

discounted cash flows and

replacement cost analysis.

During the last three years, we

completed the following

significant acquisitions:

• In September 2009, we

acquired Custom House for

$371.0 million.

• In February 2009, we acquired

the money transfer business of

FEXCO for $243.6 million.

See Note 4, Acquisitions,tothe

Notes to the Consolidated

Financial Statements, included in

Item 8, of this Annual Report on

Form 10-K, for more information

related to the purchase price

allocations for acquisitions

completed during the last three

years.

If estimates or assumptions used

to complete the purchase price

allocation and estimate the fair

value of acquired assets and

liabilities significantly differed

from assumptions made, the

allocation of purchase price

between goodwill and intangibles

could significantly differ. Such a

difference would impact future

earnings through amortization

expense of these intangibles. In

addition, if forecasts supporting

the valuation of the intangibles or

goodwill are not achieved,

impairments could arise, as

discussed further in “Goodwill

Impairment Testing” and “Other

Intangible Assets” above. For all

of our acquisitions during the

three years ended December 31,

2010, goodwill of $496.2 million

and intangibles of $208.7 million

were recognized.

69