Western Union 2010 Annual Report Download - page 106

Download and view the complete annual report

Please find page 106 of the 2010 Western Union annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

The Company administers more than 20 defined contribution plans in various countries globally on behalf of

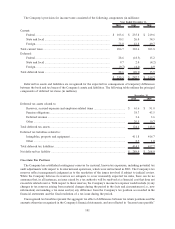

approximately 1,000 employee participants as of December 31, 2010. Such plans have vesting and employer

contribution provisions that vary by country.

In addition, the Company sponsors a non-qualified deferred compensation plan for a select group of highly

compensated employees. The plan provides tax-deferred contributions, matching and the restoration of Company

matching contributions otherwise limited under the 401(k).

The aggregate amount charged to expense in connection with all of the above plans was $12.0 million,

$11.2 million and $12.5 million during the years ended December 31, 2010, 2009 and 2008, respectively.

Defined Benefit Plan

On December 31, 2010, the Company merged its two frozen defined benefit pension plans into one plan

(“Plan”). The Plan assets were held in a master trust and were identical in terms of their benefit entitlements and

other provisions (except for participant eligibility requirements) and consequently, the financial effect of the merger

was not significant.

The Plan had a recorded unfunded pension obligation of $112.8 million as of December 31, 2010, included in

“Other liabilities” in the Consolidated Balance Sheets. In the year ended December 31, 2010, the Company made

approximately $25 million in contributions to the Plan, including a discretionary contribution of $10 million. Due to

the closure of one of its facilities in Missouri (see Note 3) and an agreement with the Pension Benefit Guaranty

Corporation, the Company funded $4.1 million during 2009. No contributions were made to the Plan during the year

ended December 31, 2008. The Company will be required to fund approximately $22 million to the Plan in 2011 and

may make a discretionary contribution of up to approximately $3 million.

The Company recognizes the funded status of the Plan in its Consolidated Balance Sheets with a corresponding

adjustment to “Accumulated other comprehensive loss,” net of tax.

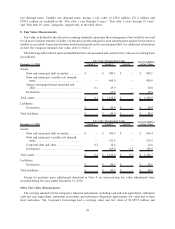

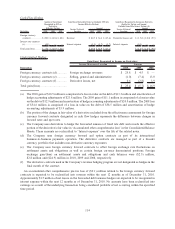

The following table provides a reconciliation of the changes in the Plan’s projected benefit obligation, fair value

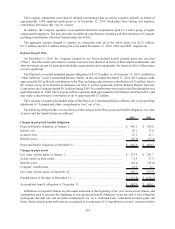

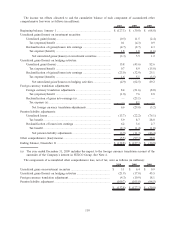

of assets and the funded status (in millions):

2010 2009

Change in projected benefit obligation

Projected benefit obligation at January 1,................................................................ $ 400.1 $ 398.8

Interest cost .......................................................................................................... 20.1 23.6

Actuarial loss ........................................................................................................ 25.3 21.1

Benefits paid......................................................................................................... (42.6) (43.4)

Projected benefit obligation at December 31, .......................................................... $ 402.9 $ 400.1

Change in plan assets

Fair value of plan assets at January 1, ..................................................................... $ 275.9 $ 291.7

Actual return on plan assets ................................................................................... 31.9 23.5

Benefits paid......................................................................................................... (42.6) (43.4)

Company contributions .......................................................................................... 24.9 4.1

Fair value of plan assets at December 31, ............................................................... 290.1 275.9

Funded status of the plan at December 31, .............................................................. $ (112.8) $ (124.2)

Accumulated benefit obligation at December 31, ..................................................... $ 402.9 $ 400.1

Differences in expected returns on plan assets estimated at the beginning of the year versus actual returns, and

assumptions used to estimate the beginning of year projected benefit obligation versus the end of year obligation

(principally discount rate and mortality assumptions) are, on a combined basis, considered actuarial gains and

losses. Such actuarial gains and losses are recognized as a component of “Comprehensive income” and amortized to

104