Western Union 2010 Annual Report Download - page 114

Download and view the complete annual report

Please find page 114 of the 2010 Western Union annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

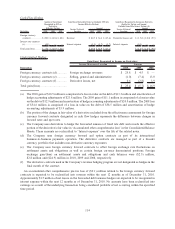

Accordingly, all changes in the fair value of the hedges not considered effective or portions of the hedge that are

excluded from the measure of effectiveness are recognized immediately in “Derivative losses, net” within the

Company’s Consolidated Statements of Income.

The Company also uses short duration foreign currency forward contracts, generally with maturities from a few

days up to one month, to offset foreign exchange rate fluctuations on settlement assets and obligations between

initiation and settlement. In addition, forward contracts, typically with maturities of less than one year, are utilized

to offset foreign exchange rate fluctuations on certain foreign currency denominated cash positions. None of these

contracts are designated as accounting hedges.

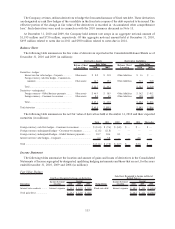

The aggregate equivalent United States dollar notional amounts of foreign currency forward contracts as of

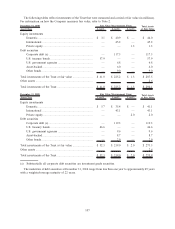

December 31, 2010 were as follows (in millions):

Contracts not designated as hedges:

Euro .................................................................................................................................. $ 206.5

British pound ..................................................................................................................... 26.6

Other ................................................................................................................................. 48.4

Contracts designated as hedges:

Euro .................................................................................................................................. $ 485.3

Canadian dollar .................................................................................................................. 107.7

British pound ..................................................................................................................... 94.3

Other ................................................................................................................................. 87.4

Foreign Currency—Global Business Payments

As a result of the acquisition of Custom House, the Company writes derivatives, primarily foreign currency forward

contracts and, to a much smaller degree, option contracts, mostly with small and medium size enterprises (customer

contracts) and derives a currency spread from this activity as part of its global business payments operations. In this

capacity, the Company facilitates cross-currency payment transactions for its customers but aggregates its Business

Solutions foreign currency exposures arising from customer contracts, including the derivative contracts described

above, and hedges the resulting net currency risks by entering into offsetting contracts with established financial

institution counterparties (economic hedge contracts). The derivatives written are part of the broader portfolio of

foreign currency positions arising from its cross-currency business-to-business payments operation, which includes

significant spot exchanges of currency in addition to forwards and options. None of these contracts are designated as

accounting hedges. The duration of these derivative contracts is generally nine months or less.

The aggregate equivalent United States dollar notional amounts of foreign currency derivative customer

contracts held by the Company as of December 31, 2010 were approximately $1.5 billion. The significant

majority of customer contracts are written in major currencies such as the Canadian dollar, euro, Australian dollar

and the British pound.

The Company has a forward contract to offset foreign exchange rate fluctuations on a Canadian dollar

denominated intercompany loan in connection with the Company’s acquisition of Custom House. This

contract, which is not designated as an accounting hedge, had a notional amount of approximately 245 million

and 230 million Canadian dollars at December 31, 2010 and December 31, 2009, respectively.

Interest Rate Hedging—Corporate

The Company utilizes interest rate swaps to effectively change the interest rate payments on a portion of its notes

from fixed-rate payments to short-term LIBOR-based variable rate payments in order to manage its overall

exposure to interest rates. The Company designates these derivatives as fair value hedges utilizing the short-cut

method, which permits an assumption of no ineffectiveness if certain criteria are met. The change in fair value of the

interest rate swaps is offset by a change in the carrying value of the debt being hedged within the Company’s

“Borrowings” in the Consolidated Balance Sheets and “Interest expense” in the Consolidated Statements of Income

has been adjusted to include the effects of interest accrued on the swaps.

112