Toyota 2015 Annual Report Download - page 128

Download and view the complete annual report

Please find page 128 of the 2015 Toyota annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

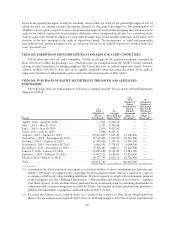

|

|

Non-U.S. Holders

The following discussion is a summary of the principal U.S. federal income tax consequences to beneficial

owners of shares of common stock or ADSs that are neither U.S. Holders, nor partnerships, nor entities taxable as

partnerships for U.S. federal income tax purposes (“Non-U.S. Holders”).

A Non-U.S. Holder generally will not be subject to any U.S. federal income or withholding tax on

distributions received in respect of shares of common stock or ADSs unless the distributions are effectively

connected with the conduct by the Non-U.S. Holder of a trade or business within the United States (and, if an

applicable tax treaty requires, are attributable to a U.S. permanent establishment or fixed base of such

Non-U.S. Holder).

A Non-U.S. Holder generally will not be subject to U.S. federal income tax in respect of gain recognized on

a sale or other disposition of shares of common stock or ADSs, unless:

(i) the gain is effectively connected with a trade or business conducted by the Non-U.S. Holder within the

United States (and, if an applicable tax treaty requires, is attributable to a U.S. permanent establishment

or fixed base of such Non-U.S. Holder); or

(ii) the Non-U.S. Holder is an individual who was present in the United States for 183 or more days in the

taxable year of the disposition and other conditions are met.

Income that is effectively connected with a U.S. trade or business of a Non-U.S. Holder, and, if an income

tax treaty applies and so requires, is attributable to a U.S. permanent establishment or fixed base of the

Non-U.S. Holder, generally will be taxed in the same manner as the income of a U.S. Holder. In addition, under

certain circumstances, any effectively connected earnings and profits realized by a corporate Non-U.S. Holder

may be subject to an additional “branch profits tax” at the rate of 30% or at a lower rate that may be prescribed

by an applicable income tax treaty.

Backup Withholding and Information Reporting

In general, information reporting requirements will apply to dividends paid to a U.S. Holder in respect of

shares of common stock or ADSs, and to the proceeds received upon the sale, exchange or redemption of the

shares of common stock or ADSs within the United States by U.S. Holders. Furthermore, backup withholding

may apply to those amounts (currently at a 28% rate) if a U.S. Holder fails to provide an accurate taxpayer

identification number to certify that such U.S. Holder is not subject to backup withholding or to otherwise

comply with the applicable requirements of the backup withholding requirements.

Dividends paid to a Non-U.S. Holder in respect of shares of common stock or ADSs, and proceeds received

upon the sale, exchange or redemption of shares of common stock or ADSs by a Non-U.S. Holder, generally are

exempt from information reporting and backup withholding under current U.S. federal income tax law. However,

a Non-U.S. Holder may be required to provide certification of non-U.S. status in order to obtain that exemption.

Persons required to establish their exempt status generally must provide such certification under penalty of

perjury on IRS Form W-9, entitled Request for Taxpayer Identification Number and Certification, in the case of

U.S. persons, and on IRS Form W-8BEN, entitled Certificate of Foreign Status of Beneficial Owner for United

States Tax Withholding and Reporting (Individuals), or IRS Form W-8BEN-E, entitled Certificate of Status of

Beneficial Owner for United States Tax Withholding and Reporting (Entities) (or other appropriate IRS Form

W-8), in the case of non-U.S. persons. Backup withholding is not an additional tax. The amount of backup

withholding imposed on a payment generally may be claimed as a credit against the holder’s U.S. federal income

tax liability, provided that the required information is properly furnished to the IRS in a timely manner.

In addition, certain U.S. Holders who are individuals that hold certain foreign financial assets (which may

include shares of common stock or ADSs) are required to report information relating to such assets, subject to

123