Sara Lee 2008 Annual Report Download - page 48

Download and view the complete annual report

Please find page 48 of the 2008 Sara Lee annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

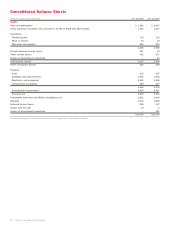

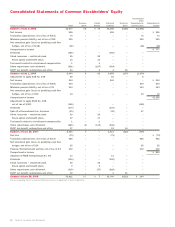

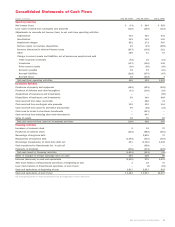

Notes to financial statements

Dollars in millions except per share data

Fixtures and Racks

Store fixtures and racks are given to retailers

to display certain of the corporation’s products. The costs of these

fixtures and racks are recognized as expense in the period in which

they are delivered to the retailer.

Advertising Expense Advertising costs, which include the

development and production of advertising materials and the com-

munication of this material through various forms of media, are

expensed in the period the advertising first takes place. Advertising

expense is recognized in the “Selling, general and administrative

expenses” line in the Consolidated Statements of Income. Total

media advertising expense for continuing operations was $325 in

2008, $313 in 2007 and $298 in 2006.

Cash and Equivalents All highly liquid investments purchased

with a maturity of three months or less at the time of purchase

are considered to be cash equivalents.

Accounts Receivable Valuation Accounts receivable are stated at

their net realizable value. The allowance for doubtful accounts reflects

the corporation’s best estimate of probable losses inherent in the

receivables portfolio determined on the basis of historical experience,

specific allowances for known troubled accounts and other currently

available information.

Shipping and Handling Costs The corporation recognizes shipping

and handling costs in the “Selling, general and administrative

expenses” line of the Consolidated Statements of Income and

recognized $703 in 2008, $656 in 2007 and $619 in 2006.

Inventory Valuation Inventories are stated at the lower of cost or

market. Cost is determined by the first-in, first-out (FIFO) method.

Rebates, discounts and other cash consideration received from a

vendor related to inventory purchases is reflected as a reduction

in the cost of the related inventory item, and is therefore, reflected

in cost of sales when the related inventory item is sold.

Recognition and Reporting of Planned Business Dispositions

When a decision to dispose of a business component is made, it

is necessary to determine how the results will be presented within

the financial statements and whether the net assets of that business

are recoverable. The following summarizes the significant accounting

policies and judgments associated with a decision to dispose

of a business.

Discontinued Operations

A discontinued operation is a business

component that meets several criteria. First, it must be possible to

clearly distinguish the operations and cash flows of the component

from other portions of the business. Second, the operations need to

have been sold or classified as held for disposal. Finally, after the

disposal, the cash flows of the component must be eliminated from

continuing operations and the corporation may not have any significant

continuing involvement in the business. Significant judgments are

involved in determining whether a business component meets the

criteria for discontinued operation reporting and the period in which

these criteria are met.

If a business component is reported as a discontinued operation,

the results of operations through the date of sale are presented on

a separate line of the income statement. Interest on corporate level

debt is not allocated to discontinued operations. Any gain or loss

recognized upon the disposition of a discontinued operation is also

reported on a separate line of the income statement. Prior to dispo-

sition, the assets and liabilities of discontinued operations are

aggregated and reported on separate lines of the balance sheet.

Gains and losses related to the sale of business components

that do not meet the discontinued operation criteria are reported

in continuing operations and separately disclosed if significant.

Businesses Held for Disposal

In order for a business to be classified

as held for disposal, several criteria must be achieved. These criteria

include, among others, an active program to market the business

and locate a buyer, as well as the probable disposition of the business

within one year. Upon being classified as held for disposal, the

recoverability of the carrying value of a business must be assessed.

Evaluating the recoverability of the assets of a business classified

as held for disposal follows a defined order in which property and

intangible assets subject to amortization are considered only after

the recoverability of goodwill, intangible assets not subject to amor-

tization and other assets are assessed. After the valuation process

is completed, the held for disposal business is reported at the lower

of its carrying value or fair value less cost to sell. The carrying value

of a held for disposal business includes the portion of the cumulative

translation adjustment related to the operation.

Businesses Held for Use

If a decision to dispose of a business is

made and the held for disposal criteria are not met, the business is

considered held for use and its assets are evaluated for recoverability

in the following order: assets other than goodwill, property and

intangibles; property and intangibles subject to amortization; and

finally, goodwill. In evaluating the recoverability of property and

intangible assets subject to amortization, in a held for use business,

the carrying value of the business is first compared to the sum of

the undiscounted cash flows expected to result from the use and

eventual disposition of the operation. If the carrying value exceeds the

undiscounted expected cash flows, then an impairment is recognized

if the carrying value of the business exceeds its fair value.

There are inherent judgments and estimates used in determining

future cash flows and it is possible that additional impairment charges

may occur in future periods. In addition, the sale of a business can

result in the recognition of a gain or loss that differs from that

anticipated prior to the closing date.

Property Property is stated at historical cost and depreciation is

computed using the straight-line method over the lives of the assets.

Machinery and equipment are depreciated over periods ranging from

3 to 25 years and buildings and building improvements over periods

of up to 40 years. Additions and improvements that substantially

extend the useful life of a particular asset and interest costs incurred

during the construction period of major properties are capitalized.

Leasehold improvements are capitalized and amortized over the

46 Sara Lee Corporation and Subsidiaries