Sara Lee 2008 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2008 Sara Lee annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

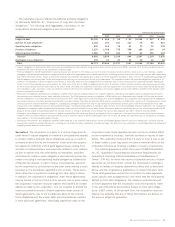

Financial review

Note 5 to the Consolidated Financial Statements sets out the

impact of the corporation’s decisions to exit the use of property in

advance of previously anticipated useful lives. Given the corporation’s

ongoing efforts to improve operating efficiency, it is reasonably likely

that future restructuring actions could result in decisions to dispose

of other assets before the end of their useful life and it is reasonably

likely that the impact of these decisions would result in impairment

and other related costs including employee severance that in the

aggregate would be significant.

Trademarks and Other Identifiable Intangible Assets The primary

identifiable intangible assets of the corporation are trademarks and

customer relationships acquired in business combinations and com-

puter software. Identifiable intangibles with finite lives are amortized

and those with indefinite lives are not amortized. The estimated

useful life of an identifiable intangible asset to the corporation is

based upon a number of factors, including the effects of demand,

competition, expected changes in distribution channels and the

level of maintenance expenditures required to obtain future cash

flows. As of June 28, 2008, the net book value of trademarks and

other identifiable intangible assets was $1,021 million, of which

$926 million is being amortized. The anticipated amortization over

the next five years is $437 million.

Identifiable intangible assets that are subject to amortization

are evaluated for impairment using a process similar to that used

to evaluate elements of property. Identifiable intangible assets not

subject to amortization are assessed for impairment at least as often

as annually and as triggering events may occur. The impairment

test for identifiable intangible assets not subject to amortization

consists of a comparison of the fair value of the intangible asset

with its carrying amount. An impairment loss is recognized for the

amount by which the carrying value exceeds the fair value of the

asset. The fair value of the intangible asset is measured using the

royalty saved method. In making this assessment, management

relies on a number of factors to discount anticipated future cash

flows including operating results, business plans and present value

techniques. Rates used to discount cash flows are dependent upon

interest rates and the cost of capital at a point in time.

There are inherent assumptions and estimates used in developing

future cash flows requiring management’s judgment in applying

these assumptions and estimates to the analysis of intangible asset

impairment including projecting revenues, interest rates, the cost

of capital, royalty rates and tax rates. Many of the factors used in

assessing fair value are outside the control of management and it

is reasonably likely that assumptions and estimates will change in

future periods. These changes can result in future impairments.

Note 3 to the Consolidated Financial Statements sets out the impact

of charges taken to recognize the impairment of intangible assets

and the factors which led to changes in estimates and assumptions.

Goodwill Goodwill is not amortized but is subject to periodic

assessments of impairment and is discussed further in Note 15.

Goodwill is assessed for impairment at least as often as annually

and as triggering events may occur. The corporation performs its

annual review in the second quarter of each year. Recoverability

of goodwill is evaluated using a two-step process. The first step

involves a comparison of the fair value of a reporting unit with its

carrying value. If the carrying value of the reporting unit exceeds

its fair value, the second step of the process involves a comparison

of the implied fair value and carrying value of the goodwill of that

reporting unit. If the carrying value of the goodwill of a reporting

unit exceeds the implied fair value of that goodwill, an impairment

loss is recognized in an amount equal to the excess. Reporting units

are business components one level below the operating segment

level for which discrete financial information is available and reviewed

by segment management. In evaluating the recoverability of goodwill,

it is necessary to estimate the fair value of the reporting units. In

making this assessment, management relies on a number of factors

to discount anticipated future cash flows including operating results,

business plans and present value techniques. Rates used to dis-

count cash flows are dependent upon interest rates and the cost

of capital at a point in time.

There are inherent assumptions and estimates used in developing

future cash flows requiring management’s judgment in applying these

assumptions and estimates to the analysis of goodwill impairment

including projecting revenues and profits, interest rates, the cost of

capital, tax rates, and the allocation of shared or corporate items.

Many of the factors used in assessing fair value are outside the

control of management and it is reasonably likely that assumptions

and estimates can change in future periods. These changes can

result in future impairments. Note 3 to the Consolidated Financial

Statements sets out the impact of charges taken to recognize the

impairment of goodwill and the factors which led to changes in

estimates and assumptions.

Self-Insurance Reserves The corporation purchases third-party

insurance for workers’ compensation, automobile and product and

general liability claims that exceed a certain level. The corporation

is responsible for the payment of claims under these insured limits,

and consulting actuaries are utilized to estimate the obligation

associated with incurred losses. Historical loss development factors

are utilized to project the future development of incurred losses, and

these amounts are adjusted based upon actual claim experience

and settlements. Consulting actuaries make a significant number of

estimates and assumptions in determining the cost to settle these

claims and many of the factors used are outside the control of the

corporation. Accordingly, it is reasonably likely that these assumptions

and estimates may change and these changes may impact future

financial results.

34 Sara Lee Corporation and Subsidiaries