Sara Lee 2008 Annual Report Download - page 31

Download and view the complete annual report

Please find page 31 of the 2008 Sara Lee annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

|

|

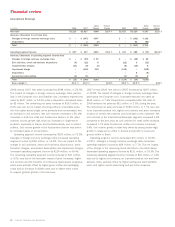

Liquidity

Notes Payable Notes payable increased from $23 million in

2007 to $280 million in 2008 as the corporation utilized short-term

borrowings to repay a portion of its maturing long-term debt. The

corporation had cash and cash equivalents on the balance sheet

at the end of 2008 and 2007 of $1,284 million and $2,517

million, respectively.

Debt The corporation’s total long-term debt decreased $1,289 million

in 2008, to $2,908 million at June 28, 2008, primarily due to the

use of cash on hand and short term borrowings to repay long-term

debt that matured during the year. The corporation’s total remaining

long-term debt of $2,908 million is due to be repaid as follows:

$568 million in 2009, $52 million in 2010, $20 million in 2011,

$1,128 million in 2012, $517 million in 2013 and $623 million

thereafter. Of the amounts that are due to be repaid in 2009, approx -

imately $394 million matures in the second quarter, $5 million

matures in the third quarter, $152 million matures in the fourth quar-

ter and the remainder matures throughout the year. Debt obligations

due to mature in the next year are expected to be satisfied with cash

on hand, cash from operating activities or with additional borrowings.

Including the impact of swaps, which are effective hedges and

convert the economic characteristics of the debt, the corporation’s

long-term debt and notes payable consist of 66.2% fixed-rate debt

as of June 28, 2008, as compared with 60.7% as of June 30, 2007.

The increase in fixed-rate debt at the end of 2008 versus the end of

2007 is due to the repayment of long-term variable rate debt during

the period and the impact of changes in foreign currency exchange

rates. The corporation monitors the interest rate environments in the

geographic regions in which it operates and modifies the components

of its debt portfolio as necessary to manage interest rate and

foreign currency risks.

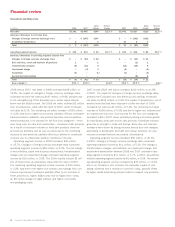

Pension Plans As shown in Note 19 to the Consolidated Financial

Statements, titled “Defined Benefit Pension Plans,” the funded status

of the corporation’s defined benefit pension plans is defined as the

amount the projected benefit obligation exceeds the plan assets.

The underfunded status of the plans is $321 million at the end of

fiscal 2008 as compared to $580 million at the end of fiscal 2007.

The corporation expects to contribute $196 million of cash to

its pension plans in 2009 as compared to $175 million in 2008,

$191 million in 2007 and $331 million in 2006. The 2009 contri-

butions are for pension plans of continuing operations and pension

plans where the corporation has agreed to retain the pension liabil-

ity after certain business dispositions were completed. The exact

amount of cash contributions made to pension plans in any year is

dependent upon a number of factors, including minimum funding

requirements in the jurisdictions in which the company operates,

the timing of cash tax benefits for amounts funded and arrangements

made with the trustees of certain foreign plans. As a result, the

actual funding in 2009 may be materially different from the estimate.

During 2006, the corporation entered into an agreement to fully

fund certain U.K. pension obligations by 2015. The anticipated 2009

contributions reflect the amounts agreed upon with the trustees of

these U.K. plans. Under the terms of this agreement, the corporation

will make annual pension contributions of 32 million British pounds

to the U.K. plans through 2015. Subsequent to 2015, the corporation

has agreed to keep the U.K. plans fully funded in accordance with

local funding standards. If at any time prior to January 1, 2016,

Sara Lee Corporation ceases having a credit rating equal to or greater

than all three of the following ratings, the annual pension funding of

these U.K. plans will increase by 20%: Standard & Poor’s minimum

credit rating of “BBB-,” Moody’s Investors Service minimum credit

rating of “Baa3” and FitchRatings minimum credit rating of “BBB-.”

The corporation’s credit ratings are currently above these levels and

are discussed below in this Liquidity section.

Repatriation of Foreign Earnings and Income Taxes Since 2006,

the corporation has adopted a policy of repatriating a higher level

of foreign sourced earnings to fund U.S. cash requirements. The

Hanesbrands business that was spun off in 2007 historically gener-

ated a significant amount of cash from operations within the U.S.,

which was used to service debt payments, dividends and other domes-

tic capital requirements. As a result of the spin off of Hanesbrands

and the disposition of a number of significant European operations,

the corporation has repatriated dividends annually since 2006 and

will likely continue to do so in the future. This policy will increase the

corporation’s income tax rate and increase cash income taxes paid.

The tax costs associated with the anticipated repatriation of

foreign earnings are recognized as the amounts are earned. However,

the corporation pays the tax liability upon completing the repatria-

tion action.

During the first quarter of 2008, the corporation repatriated

$1.4 billion of foreign accumulated earnings to the U.S. The taxes

paid on the $1.4 billion dividend were fully accrued in 2007 and prior

years. This dividend, in isolation, would have required the payment

of approximately $420 million of cash taxes over the remainder of

2008. However, other income or losses generated by the business

impacted the ultimate amount of 2008 cash taxes paid. During 2008

the corporation accrued $125 million of taxes payable relating to the

repatriation of $720 million of 2008 foreign earnings. This repatria-

tion, in isolation, will result in a payment of $125 million of cash

tax in 2009. However, other income or losses generated by the

business will impact the ultimate cash tax payment.

Sara Lee Corporation and Subsidiaries 29