Pitney Bowes 2013 Annual Report Download - page 90

Download and view the complete annual report

Please find page 90 of the 2013 Pitney Bowes annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

PITNEY BOWES INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Tabular dollars in thousands, except per share amounts)

79

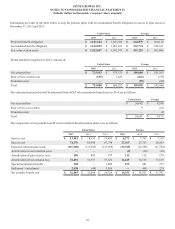

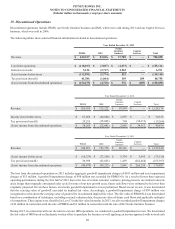

Other changes in plan assets and benefit obligations for defined benefit pension plans recognized in other comprehensive income were

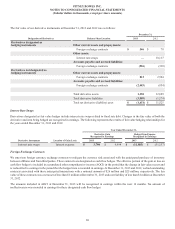

as follows:

United States Foreign

2013 2012 2013 2012

Net actuarial (gain) loss $(111,232)$ 73,701 $(29,320)$ 32,596

Prior service credit —(127)——

Amortization of net actuarial loss (32,494)(52,957)(14,445)(14,103)

Amortization of prior service cost (380)(803)(112)(112)

Net transition asset ——910

Settlement / curtailment (2,638)48 —(444)

Total recognized in other comprehensive income $(146,744)$ 19,862 $(43,868)$ 17,947

Weighted-average actuarial assumptions used to determine end of year benefit obligations and net periodic benefit cost for defined benefit

pension plans include:

2013 2012 2011

United States

Used to determine benefit obligations

Discount rate 4.95% 4.05% 4.95%

Rate of compensation increase 3.50% 3.50% 3.50%

Used to determine net periodic benefit cost

Discount rate 4.05% 4.95% 5.60%

Expected return on plan assets 7.25% 7.75% 8.00%

Rate of compensation increase 3.50% 3.50% 3.50%

Foreign

Used to determine benefit obligations

Discount rate 1.45% - 4.60% 1.95% - 4.65% 1.80% - 6.10%

Rate of compensation increase 1.50% - 3.50% 1.50% - 3.50% 2.10% - 4.60%

Used to determine net periodic benefit cost

Discount rate 1.95% - 4.65% 1.80% - 6.10% 2.00% - 5.50%

Expected return on plan assets 3.50% - 7.50% 3.25% - 7.50% 4.00% - 7.75%

Rate of compensation increase 1.50% - 3.50% 2.10% - 4.60% 2.10% - 5.50%

A discount rate is used to determine the present value of our future benefit obligations. The discount rate for our U.S. pension and

postretirement medical benefit plans is determined by matching the expected cash flows associated with our benefit obligations to a yield

curve based on long-term, high-quality fixed income debt instruments available as of the measurement date. For the U.K. retirement

benefit plan, our largest foreign plan, the discount rate is determined by discounting each year's estimated benefit payments by an applicable

spot rate, derived from a yield curve created from a large number of high-quality corporate bonds. For our other smaller foreign pension

plans, the discount rate is selected based on high-quality fixed income indices available in the country in which the plan is domiciled.

The expected return on plan assets is based on historical and expected rates of return for current and planned asset classes in the plans'

investment portfolio after analyzing historical experience and future expectations of the returns and volatility of the various asset classes.

The overall expected rate of return for the portfolio is based on the asset allocation at the end of the year for our U.S. pension plans and

the target asset allocation for our international pension plans, adjusted for historical and expected experience of active portfolio

management results, when compared to the benchmark returns. When assessing the expected future returns for the portfolio, management

places more emphasis on the expected future returns than historical returns.