Pitney Bowes 2013 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2013 Pitney Bowes annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

PITNEY BOWES INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Tabular dollars in thousands, except per share amounts)

68

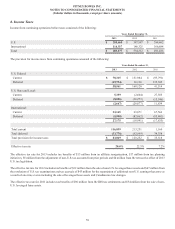

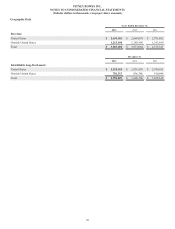

Available-For-Sale Securities

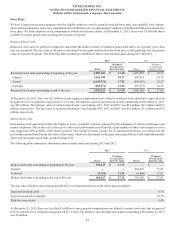

At December 31, 2013 and 2012, available-for-sale securities consisted of the following:

December 31, 2013

Amortized cost

Gross

unrealized

gains

Gross

unrealized

losses

Estimated fair

value

U.S. and foreign governments, agencies and municipalities 121,803 999 (3,372) 119,430

Corporate 37,901 935 (572) 38,264

Mortgage-backed / asset-backed securities 165,664 1,570 (2,636) 164,598

Total $ 325,368 $ 3,504 $ (6,580) $ 322,292

December 31, 2012

Amortized cost

Gross unrealized

gains

Gross unrealized

losses

Estimated fair

value

U.S. and foreign governments, agencies and municipalities 127,807 3,972 (56) 131,723

Corporate 41,095 2,851 (20) 43,926

Mortgage-backed / asset-backed securities 162,180 3,340 (3,145) 162,375

Total $ 331,082 $ 10,163 $ (3,221) $ 338,024

Gross unrealized losses on investment securities that were in a loss position for greater than 12 months were $1 million at December 31,

2013 and less than $1 million at December 31, 2012. We have not recognized an other-than-temporary impairment on any of the investment

securities in an unrealized loss position because we do not intend to sell these securities, it is more likely than not that we will not be

required to sell these securities before recovery of the unrealized losses and we expect to receive the contractual principal and interest

on these investment securities.

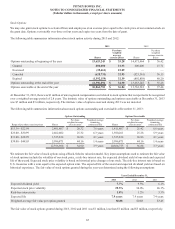

At December 31, 2013, the amortized cost and estimated fair value of available-for-sale securities have scheduled maturities as follows:

Amortized cost

Estimated fair

value

Within 1 year $ 41,853 $ 41,932

After 1 year through 5 years 46,869 47,284

After 5 years through 10 years 67,160 66,140

After 10 years 169,486 166,936

Total $ 325,368 $ 322,292

The expected payments on mortgage-backed and asset-backed securities may not coincide with their contractual maturities as borrowers

have the right to prepay obligations with or without prepayment penalties.

We have not experienced any write-offs in our investment portfolio. The majority of our mortgage-backed securities are either guaranteed

or supported by the U.S. government. We have no investments in inactive markets that would warrant a possible change in our pricing

methods or classification within the fair value hierarchy. Further, we have no investments in auction rate securities.

Derivative Instruments

The valuation of foreign exchange derivatives is based on a market approach using observable market inputs, such as forward rates. The

valuation of interest rate swaps is based on an income approach using a model with inputs that are observable or that can be derived from

or corroborated by observable market data. As required by the fair value measurements guidance, we also incorporate counterparty credit

risk and our credit risk into the fair value measurement of our derivative assets and liabilities, respectively. We derive credit risk from

observable data related to credit default swaps.

$ $ $ $

$ $ $ $