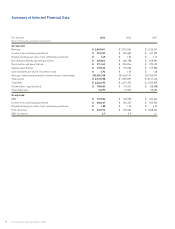

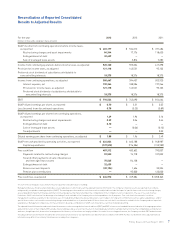

Pitney Bowes 2013 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 2013 Pitney Bowes annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

6

Digital Commerce Solutions

The Digital Commerce Solutions segment operates in several highly competitive and rapidly evolving markets. We face competition

from large global companies that offer a broad range of solutions to smaller, more narrowly-focused companies that can design very

targeted solutions. The principal competitive factors in this segment include reliability, functionality and ease of use, scalability, innovation,

support services and price. We compete in this segment based on the accuracy and processing speed of our solutions, particularly those

used in our location intelligence and e-commerce parcel management solutions. The breadth and scalability of our products and solutions,

our single-sourced geocoding and reverse geocoding capabilities, and our ability to identify rapidly changing customer needs and

requirements and develop technologies and solutions to meet these changing needs and requirements are also key factors.

Our direct marketing services products compete for a portion of our clients' overall marketing budget by demonstrating the value of our

products and services relative to other marketing programs available to our advertising clients.

Customer Financing

We offer a variety of finance and payment solutions to our clients to finance their equipment and product purchases, rental and lease

payments, postage replenishment and supplies purchases. We establish credit approval limits and procedures based on the credit quality

of the client and the type of product or service provided to control risk in extending credit to clients. In addition, we utilize an automatic

approval program for certain leases. This program is designed to facilitate low dollar transactions by utilizing historical payment patterns

and losses realized for clients with common credit characteristics. The program defines the criteria under which we will accept a client

without performing a more detailed credit investigation, such as maximum equipment cost, a client's time in business and payment

experience.

We closely monitor the portfolio by analyzing industry sectors and delinquency trends by product line, industry and client to ensure

reserve levels and credit policies reflect current trends. Management continues to closely monitor credit lines and collection resources

We provide financing solutions to our clients through the Bank. The Bank's key product offering, Purchase Power, is a revolving credit

solution, which enables clients to rent, lease or purchase products, supplies and services. The Bank also provides a deposit solution to

those clients that prefer to prepay postage and earn interest on their deposits. The Bank is regulated by the Federal Deposit Insurance

Corporation (FDIC) and the Utah Department of Financial Institutions. The Bank's assets consist primarily of cash, finance receivables

and investments and liabilities consist primarily of deposit accounts. At December 31, 2013 and December 31, 2012, the Bank had assets

of $779 million and $796 million, respectively, and liabilities of $734 million and $733 million, respectively.

Our financing operations face competition, in varying degrees, from large, diversified financial institutions, including leasing companies,

commercial finance companies and commercial banks, to small, specialized firms.

Research, Development and Intellectual Property

We invest in research and development programs to develop new products and service offerings and deliver high value technology,

innovative software and differentiated services in high value segments of the market. We will continue to invest a substantial percentage

of our total research and development budget in the growth areas of our business to develop, among other things, new customer engagement,

location intelligence and e-commerce cross-border parcel management solutions. Our expenditures for research and development were

$110 million, $114 million and $129 million in 2013, 2012 and 2011, respectively.

As a result of our research and development efforts, we have been awarded a number of patents with respect to several of our existing

and planned products. We do not believe our businesses are materially dependent on any one patent or license or any group of related

patents or group of related licenses.

Material Suppliers

We depend on third-party suppliers for a variety of services, components, supplies and a large portion of our product manufacturing. In

certain instances, we rely on single sourced or limited sourced suppliers around the world because the relationship is advantageous due

to quality, price, or there are no alternative sources. We have not historically experienced shortages in services, components or products

and believe that our available sources for materials, components, services and supplies are adequate.

Regulatory Matters

We are subject to the regulations of postal authorities worldwide related to product specifications and business practices involving our

postage meters.

and revise credit policies as necessary to be more selective in managing the portfolio.