Pitney Bowes 2013 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2013 Pitney Bowes annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

|

|

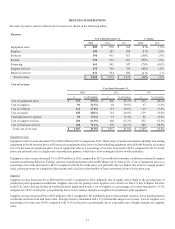

25

(1) Interest payments on debt assume all debt is held to maturity. Certain notes permit us to redeem, or the bondholders to require us to

redeem, some or all of the applicable outstanding notes at par plus accrued interest before the scheduled maturity date.

(2) Purchase obligations include unrecorded agreements to purchase goods or services that are enforceable and legally binding upon us

and that specify all significant terms, including fixed or minimum quantities to be purchased; fixed, minimum or variable price

provisions; and the approximate timing of the transaction. Purchase obligations exclude agreements that are cancelable without

penalty.

(3) Represents the amount of contributions we anticipate making to our pension plans during 2014; however, we will assess our funding

alternatives as the year progresses.

(4) Our retiree health benefit plans are non-funded plans and cash contributions are made each year to cover medical claims costs

incurred. The amounts reported in the above table represent our estimate of future benefits payments.

Critical Accounting Estimates

The preparation of our financial statements in conformity with GAAP requires management to make estimates and assumptions about

certain items that affect the reported amounts of assets, liabilities, revenues, expenses and accompanying disclosures, including the

disclosure of contingent assets and liabilities. The accounting policies below have been identified by management as those accounting

policies that are most critical to our financial statements due to the estimates and assumptions required. Management believes that the

estimates and assumptions used are reasonable and appropriate based on the information available at the time the financial statements

were prepared; however, actual results could differ from those estimates and assumptions. See Note 1 to the Consolidated Financial

Statements for a summary of our accounting policies.

Revenue recognition - Multiple element arrangements

We derive revenue from multiple sources including sales, rentals, financing and services. Certain transactions are consummated at the

same time and can therefore generate revenue from multiple sources. The most common form of these transactions involves a sale or

non-cancelable lease of equipment, a meter rental and an equipment maintenance agreement. As a result, we are required to determine

whether the deliverables in a multiple element arrangement should be treated as separate units of accounting for revenue recognition

purposes, and if so, how the price should be allocated among the delivered elements and when to recognize revenue for each element.

We recognize revenue for delivered elements only when the fair values of undelivered elements are known, customer acceptance has

occurred and payment is probable.

In these multiple element arrangements, revenue is allocated to each of the elements based on relative “selling prices” and the selling

price for each of the elements is determined based on vendor specific objective evidence. We establish vendor specific objective evidence

of selling prices for our products and services based on the prices charged for each element when sold separately in standalone transactions.

The allocation of relative selling price to the various elements impacts the timing of revenue recognition, but does not change the total

revenue recognized. Revenue is allocated to the meter rental and equipment maintenance agreement elements using their respective

selling prices charged in standalone and renewal transactions. For a sale transaction, revenue is allocated to the equipment based on a

range of selling prices in standalone transactions. For a lease transaction, revenue is allocated to the equipment based on the present value

of the remaining minimum lease payments. The amount allocated to equipment is compared to the range of selling prices in standalone

transactions during the period to ensure the allocated equipment amount approximates average selling prices.

Pension benefits

The valuation of our pension assets and obligations and the calculation of net periodic pension expense are dependent on assumptions

and estimates relating to, among other things, the interest rate used to discount the future estimated liability (discount rate) and the

expected rate of return on plan assets. These assumptions are evaluated and updated annually and are described in further detail in Note

18 to the Consolidated Financial Statements.

The discount rate for our largest plan, the U.S. Qualified Pension Plan (the U.S. Plan) is determined by matching the expected cash flows

associated with our benefit obligations to a yield curve based on long-term, high quality fixed income debt instruments available as of

the measurement date. The discount rate for our largest foreign plan, the U.K. Qualified Pension Plan (the U.K. Plan), is determined by

using a model that discounts each year's estimated benefit payments by an applicable spot rate derived from a yield curve created from

a large number of high quality corporate bonds. The discount rate used in the determination of net periodic pension expense for 2013

was 4.05% for the U.S. Plan and 4.55% for the U.K. Plan. For 2014, the discount rate used in the determination of net periodic pension

expense for the U.S. Plan and the U.K. Plan will be 4.95% and 4.45%, respectively. A 0.25% increase in the discount rate would decrease