Pitney Bowes 2011 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2011 Pitney Bowes annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

|

|

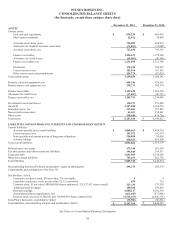

PITNEY BOWES INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Tabular dollars in thousands, except per share data)

42

for rental equipment and three to five years for computer equipment. Major improvements which add to productive capacity or extend

the life of an asset are capitalized while repairs and maintenance are charged to expense as incurred. Leasehold improvements are

amortized over the shorter of the estimated useful life or their related lease term.

Fully depreciated assets are retained in fixed assets and accumulated depreciation until they are removed from service. In the case of

disposals, assets and related accumulated depreciation are removed from the accounts, and the net amounts, less proceeds from

disposal, are included in earnings.

Software Development Costs

We capitalize certain costs of software developed for internal use. Capitalized costs include purchased materials and services, payroll

and personnel-related costs and interest costs. The cost of internally developed software is amortized on a straight-line basis over its

estimated useful life, principally three to 10 years.

Costs incurred for the development of software to be sold, leased, or otherwise marketed are expensed as incurred until technological

feasibility has been established, at which time such costs are capitalized until the product is available for general release to the public.

Capitalized software development costs include purchased materials and services, and payroll and personnel-related costs attributable

to programmers, software engineers, quality control and field certifiers. Capitalized software development costs are amortized over

the product’s estimated useful life, principally three to five years, generally on a straight-line basis. Amortization of capitalized

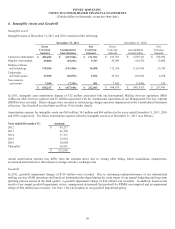

software development costs were $10 million, $8 million and $10 million for the years ended December 31, 2011, 2010, and 2009,

respectively. Other assets include $14 and $20 million of capitalized software development costs at December 31, 2011 and 2010,

respectively. Software development costs capitalized in 2011 and 2010 were $5 million and $6 million, respectively.

Research and Development Costs

Research and product development costs are expensed as incurred. These costs primarily include personnel-related costs.

Business Combinations

We account for business combinations using the acquisition method of accounting, which requires that the assets acquired and

liabilities assumed be recorded at the date of acquisition at their respective fair values. The fair value of intangible assets is estimated

using a cost, market or income approach. Goodwill represents the excess of the purchase price over the estimated fair values of net

tangible and intangible assets acquired. Finite-lived intangible assets are amortized over their estimated useful lives, principally three

to 15 years, using either the straight-line method or an accelerated attrition method.

Impairment Review for Long-lived Assets

Long-lived assets are reviewed for impairment on an annual basis or whenever events or changes in circumstances indicate that the

carrying amount may not be fully recoverable. If such a change in circumstances occurs, the related estimated future undiscounted

cash flows expected to result from the use of the asset and its eventual disposition is compared to the carrying amount. If the sum of

the expected cash flows is less than the carrying amount, an impairment charge is recorded. The impairment charge is measured as the

amount by which the carrying amount exceeds the fair value of the asset. The fair value of the impaired asset is determined using

probability weighted expected cash flow estimates, quoted market prices when available and appraisals, as appropriate.

Impairment Review for Goodwill and Intangible Assets

Goodwill is tested annually for impairment, during the fourth quarter, or sooner when circumstances indicate an impairment may

exist, at the reporting unit level. A reporting unit is the operating segment, or a business, which is one level below that operating

segment. Reporting units are aggregated as a single reporting unit if they have similar economic characteristics. Goodwill is tested

for impairment using a two-step approach. In the first step, the fair value of each reporting unit is determined. If the fair value of a

reporting unit is less than its carrying value, the second step of the goodwill impairment test is performed to measure the amount of

impairment, if any. In the second step, the fair value of the reporting unit is allocated to the assets and liabilities of the reporting unit

as if it had been acquired in a business combination and the purchase price was equivalent to the fair value of the reporting unit. The

excess of the fair value of the reporting unit over the amounts assigned to its assets and liabilities is referred to as the implied fair

value of goodwill. The implied fair value of the reporting unit’s goodwill is then compared to the actual carrying value of goodwill.

If the implied fair value of goodwill is less than the carrying value of goodwill, an impairment loss is recognized for the difference.

The fair value of a reporting unit is determined based on a combination of various techniques, including the present value of future

cash flows, multiples of competitors and multiples from sales of like businesses.

Intangible assets are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount may not

be fully recoverable. If such a change in circumstances occurs, the related estimated future undiscounted cash flows expected to result

from the use of the asset and its eventual disposition is compared to the carrying amount. If the sum of the expected cash flows is less