Pep Boys 2013 Annual Report Download - page 144

Download and view the complete annual report

Please find page 144 of the 2013 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

THE PEP BOYS—MANNY, MOE & JACK AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Years ended February 1, 2014, February 2, 2013 and January 28, 2012

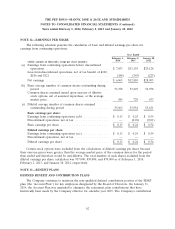

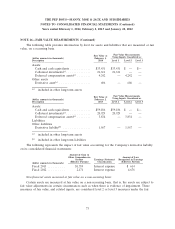

NOTE 16—FAIR VALUE MEASUREMENTS (Continued)

inputs and minimizes the use of unobservable inputs by requiring that the most observable inputs be

used when available. Observable inputs are inputs market participants would use in valuing the asset or

liability developed based on market data obtained from sources independent of the Company.

Unobservable inputs are inputs that reflect the Company’s assumptions about the factors market

participants would use in valuing the asset or liability developed based upon the best information

available in the circumstances. The hierarchy is broken down into three levels. Level 1 inputs are

quoted prices (unadjusted) in active markets for identical assets or liabilities. Level 2 inputs include

quoted prices for similar assets or liabilities in active markets. Level 3 inputs are unobservable inputs

for the asset or liability. Categorization within the valuation hierarchy is based upon the lowest level of

input that is significant to the fair value measurement.

Assets and Liabilities that are Measured at Fair Value on a Recurring Basis:

The Company’s long-term investments and interest rate swap agreements are measured at fair

value on a recurring basis. The information in the following paragraphs and tables primarily addresses

matters relative to these assets and liabilities.

Cash equivalents:

Cash equivalents, other than credit card receivables, include highly liquid investments with an

original maturity of three months or less at acquisition. The Company carries these investments at fair

value. As a result, the Company has determined that its cash equivalents in their entirety are classified

as a Level 1 measure within the fair value hierarchy.

Collateral investments:

Collateral investments include monies on deposit that are restricted. The Company carries these

investments at fair value. As a result, the Company has determined that its collateral investments are

classified as a Level 1 measure within the fair value hierarchy.

Deferred compensation assets:

Deferred compensation assets include variable life insurance policies held in a Rabbi Trust. The

Company values these policies using observable market data. The inputs used to value the variable life

insurance policy fall within Level 2 of the fair value hierarchy.

Derivative liability:

The Company has two interest rate swaps designated as cash flow hedges on $100.0 million of the

Company’s Senior Secured Term Loan facility that expires in October 2018. The Company values this

swap using observable market data to discount projected cash flows and for credit risk adjustments.

The inputs used to value derivatives fall within Level 2 of the fair value hierarchy.

72