Pep Boys 2013 Annual Report Download - page 138

Download and view the complete annual report

Please find page 138 of the 2013 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

THE PEP BOYS—MANNY, MOE & JACK AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Years ended February 1, 2014, February 2, 2013 and January 28, 2012

NOTE 13—BENEFIT PLANS (Continued)

the Plan was to meet current and future benefit payment needs within the constraints of diversification

and prudent risk taking. The Plan was diversified across asset classes to achieve an optimal balance

between risk and return and between income and growth of assets through capital appreciation.

Investment objectives for each asset class were determined based on specific risks and investment

opportunities identified. The Company believes that the diversification of its assets minimizes the risk

due to concentration of the Plan assets.

The Company updated its long-term, strategic asset allocations annually using various analytics to

determine the optimal asset mix and consideration of plan liability characteristics, liquidity

characteristics, funding requirements, expected rates of return and the distribution of returns. Actual

allocations to each asset class vary from target allocations due to periodic investment strategy changes,

market value fluctuations, the length of time it takes to fully implement investment allocation positions

(such as private equity and real estate), and the timing of benefit payments and contributions. Short

term investments and exchange-traded derivatives were used to rebalance the actual asset allocation to

the target asset allocation. The asset allocation was monitored and rebalanced on a monthly basis.

The manager of the investments provided advice and recommendations to help the Committee

discharge its fiduciary responsibilities in furtherance of the Plan’s goals and objectives. The manager

had the discretion to allocate assets among funds within each asset class to conform to strategic targets

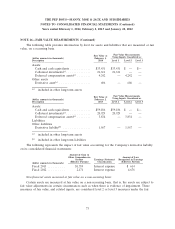

and ranges established by the Committee. The target asset allocation was 50% equity securities and

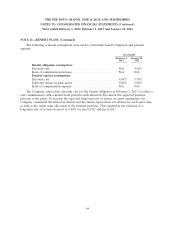

50% fixed income. The investment policy requires that the asset allocation be maintained within certain

ranges. The weighted average asset allocations and asset allocation ranges by asset category were as

follows:

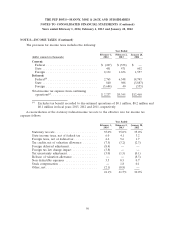

Weighted Average Asset Allocations

January 28, Asset Allocation

2012 Ranges

Total equities ................................. 50% 45 - 55%

Domestic equities ............................ 32% 28 - 38%

Non-US equities ............................. 18% 12 - 22%

Fixed income ................................. 50% 45 - 55%

Generally, investments are valued based on information in financial publications of general

circulation, statistical and valuation services, records of security exchanges, appraisal by qualified

persons, transactions and bona fide offers. Money market funds are valued using a market approach

based on the quoted market prices of identical instruments. These investments are classified within

Level 1 of the fair value hierarchy.

Domestic equities, non-US equities, and both long duration fixed income securities consist of

collective trust (‘‘CT’’) funds. CT funds are comprised of shares or units in commingled funds that are

not publicly traded. The underlying assets in these funds (equity securities and fixed income securities)

are publicly traded on exchanges and price quotes for the assets held by these funds are readily

available. CT funds are valued at their net asset values that are calculated by the investment manager

of the fund and have daily or monthly liquidity. These investments are classified within Level 2 of the

fair value hierarchy.

66