Pep Boys 2009 Annual Report Download - page 95

Download and view the complete annual report

Please find page 95 of the 2009 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

ITEM 7A QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

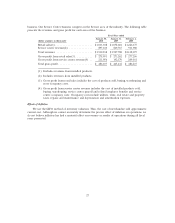

The Company has market rate exposure in its financial instruments due to changes in interest

rates.

Variable and Fixed Rate Debt

The Company’s Revolving Credit Agreement bears interest at LIBOR or Prime plus 2.75% to

3.25% based upon the then current availability under the facility. At January 30, 2010, there were no

outstanding borrowings under the agreement. Additionally, the Company has a Senior Secured Term

Loan facility with a balance of $149,715,000 at January 30, 2010, that bears interest at three month

LIBOR plus 2.00%. Excluding our interest rate swap, a one percent change in the LIBOR rate would

have affected net earnings by approximately $1.0 million for fiscal 2009.

At January 30, 2010, the fair value of the Company’s fixed rate debt instruments, principally the

$157,565,000 7.50% Senior Subordinated Notes, due December 15, 2014,was $148,899,000.

At January 31, 2009, the Company had outstanding $179,050,000 of fixed rate notes with an

aggregate fair market value of $84,301,000. The Company determines fair value on its fixed rate debt

by using quoted market prices and current interest rates.

Interest Rate Swaps

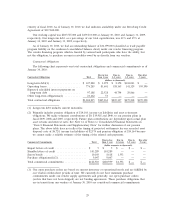

On November 2, 2006, the Company entered into an interest rate swap for a notional amount of

$200,000,000. The Company has designated the swap a cash flow hedge on the first $200,000,000 of the

Company’s $320,000,000 Senior Secured Tem Loan facility. The interest rate swap converts the variable

LIBOR portion of the interest payments to a fixed rate of 5.036% and terminates in October 2013.

On November 27, 2007, the Company sold the land and buildings for 34 owned properties to an

independent third party. The Company used $162,558,000 of the net proceeds from the transaction to

prepay a portion of the Senior Secured Term Loan facility which eliminated a portion of the future

interest payments hedged by the November 2, 2006 interest rate swap. The Company discontinued

hedge accounting for the unmatched portion of the November 2, 2006 swap and reclassified a

$2,259,000 pre-tax loss from other comprehensive income to interest expense. On November 27, 2007,

the Company re-designated $145,000,000 notional amount of the interest rate swap as a cash flow

hedge to fully match the future interest payments under the Senior Secured Term Loan facility. As a

result, all future changes in the fair value of this interest rate swap that has been re-designated as a

hedge will be recorded to accumulated other comprehensive loss. From the period of November 27,

2007 through February 1, 2008 the Company incurred interest expense of $1,907,000 for changes in fair

value related to the $55,000,000 unmatched portion of this swap. On February 1, 2008, the Company

recorded $4,539,000 within accrued expenses to reduce the notional amount of the interest rate swap to

$145,000,000 from the original $200,000,000 amount. The $4,539,000 was paid on February 4, 2008. As

of January 30, 2010 and January 31, 2009, respectively, the fair value of the swap was a net $16,401,000

and $15,808,000 payable recorded within other long-term liabilities on the balance sheet.

37