Pep Boys 2009 Annual Report Download - page 93

Download and view the complete annual report

Please find page 93 of the 2009 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

|

|

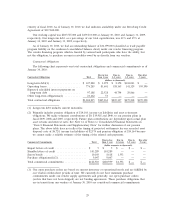

court cases, and outcomes of tax audits. To the extent our actual tax liability differs from our

established tax liabilities for unrecognized tax benefits, our effective tax rate may be materially

impacted. While it is often difficult to predict the final outcome of, the timing of, or the tax

treatment of any particular tax position or deduction, we believe that our tax balances reflect the

more-likely-than-not outcome of known tax contingencies.

The temporary differences between the book and tax treatment of income and expenses result in

deferred tax assets and liabilities, which are included within our consolidated balance sheets. We

must then assess the likelihood that our deferred tax assets will be recovered from future taxable

income. To the extent we believe that recovery is not more-likely-than-not, we must establish a

valuation allowance. In this regard when determining whether or not we should establish a

valuation allowance, the Company considers various tax planning strategies, including potential

real estate transactions, as future taxable income. To the extent we establish a valuation

allowance or change the allowance in a future period, income tax expense will be impacted.

Actual results could differ from this assessment if adequate taxable income is not generated in

future periods from either operations or projected tax planning strategies. We had net deferred

tax assets of $28,187,000 and $41,860,000 as of January 30, 2010 and January 31, 2009,

respectively.

35