Nike 2003 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2003 Nike annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74

|

|

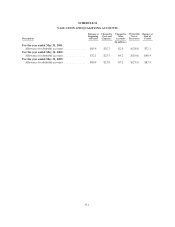

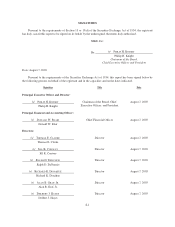

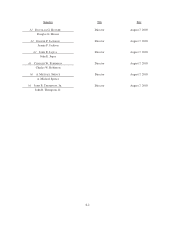

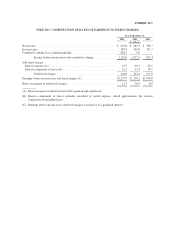

Item 9. Changes In and Disagreements with Accountants on Accounting and Financial Disclosure

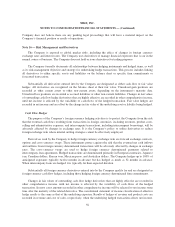

There has been no change of accountants nor any disagreements with accountants on any matter of

accounting principles or practices or financial statement disclosure required to be reported under this Item.

Item 9A. Controls and Procedures

The Company maintains disclosure controls and procedures that are designed to ensure that information

required to be disclosed in the Company’s Exchange Act reports is recorded, processed, summarized and

reported within the time periods specified in the Securities and Exchange Commission’s rules and forms and that

such information is accumulated and communicated to the Company’s management, including its Chief

Executive Officer and Chief Financial Officer, as appropriate, to allow for timely decisions regarding required

disclosure. In designing and evaluating the disclosure controls and procedures, management recognizes that any

controls and procedures, no matter how well designed and operated, can provide only reasonable assurance of

achieving the desired control objectives, and management is required to apply its judgment in evaluating the

cost-benefit relationship of possible controls and procedures.

The Company carries out a variety of on-going procedures, under the supervision and with the participation

of the Company’s management, including the Chief Executive Officer and the Company’s Chief Financial

Officer, to evaluate the effectiveness of the design and operation of the Company’s disclosure controls and

procedures. Based on the foregoing, the Company’s Chief Executive Officer and Chief Financial Officer

concluded that the Company’s disclosure controls and procedures were effective at the reasonable assurance

level as of May 31, 2003.

There has been no change in the Company’s internal controls over financial reporting during the Company’s

most recent fiscal quarter that has materially affected, or is reasonable likely to materially affect, the Company’s

internal controls over financial reporting.

63