Nike 2003 Annual Report Download - page 17

Download and view the complete annual report

Please find page 17 of the 2003 Nike annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

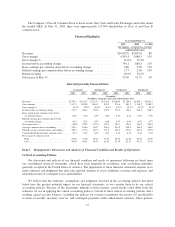

|

|

require that we make estimates in the preparation of our financial statements as of a given date. However, since

our business cycle is relatively short, actual results related to these estimates are generally known within the six-

month period following the financial statement date. Thus, these policies generally affect only the timing of

reported amounts across two to three quarters.

Within the context of these critical accounting policies, we are not currently aware of any reasonably likely

events or circumstances that would result in materially different amounts being reported.

Revenue Recognition

We record wholesale revenues when title passes and the risks and rewards of ownership have passed to the

customer, based on the terms of sale. Title passes generally upon shipment or upon receipt by the customer

depending on the country of the sale and the agreement with the customer. Retail store revenues are recorded at

the time of sale.

In some instances, we ship product directly from our supplier to the customer. In these cases, we recognize

revenue when the product is delivered to and accepted by the customer. Our revenues may fluctuate in cases

when our customers delay accepting shipment of product for periods up to several weeks.

In certain countries outside of the U.S., precise information regarding the date of receipt by the customer is

not readily available. In these cases, we estimate the date of receipt by the customer based upon historical

delivery times by geographic location. On the basis of our tests of actual transactions, we have no indication that

these estimates have been materially inaccurate historically.

As part of our revenue recognition policy, we record estimated sales returns and miscellaneous claims from

customers as reductions to revenues at the time revenues are recorded. We base our estimates on historical rates

of product returns and claims, and specific identification of outstanding claims and outstanding returns not yet

received from customers. Actual returns and claims in any future period are inherently uncertain and thus may

differ from our estimates. If actual or expected future returns and claims were significantly greater or lower than

the reserves we had established, we would record a reduction or increase to net revenues in the period in which

we made such determination.

Reserve for Uncollectible Accounts Receivable

We make ongoing estimates relating to the collectibility of our accounts receivable and maintain a reserve

for estimated losses resulting from the inability of our customers to make required payments. In determining the

amount of the reserve, we consider our historical level of credit losses and make judgments about the

creditworthiness of significant customers based on ongoing credit evaluations. Since we cannot predict future

changes in the financial stability of our customers, actual future losses from uncollectible accounts may differ

from our estimates. If the financial condition of our customers were to deteriorate, resulting in their inability to

make payments, a larger reserve might be required. In the event we determined that a smaller or larger reserve

was appropriate, we would record a credit or a charge to selling and administrative expense in the period in

which we made such a determination.

Inventory Reserves

We also make ongoing estimates relating to the net realizable value of inventories, based upon our

assumptions about future demand and market conditions. If we estimate that the net realizable value of our

inventory is less than the cost of the inventory recorded on our books, we record a reserve equal to the difference

between the cost of the inventory and the estimated net realizable value. This reserve is recorded as a charge to

cost of sales. If changes in market conditions result in reductions in the estimated net realizable value of our

inventory below our previous estimate, we would increase our reserve in the period in which we made such a

determination and record a charge to cost of sales.

16