NetSpend 2010 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2010 NetSpend annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

|

|

Table of Contents

term loan and our initial draw of $10.0 million under the revolving credit facility to fund the dividend paid in connection with the Skylight

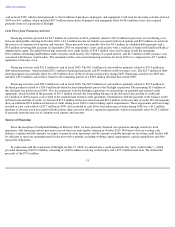

acquisition as well as closing costs of the Skylight acquisition, including retiring $40.4 million of existing Skylight debt and refinancing our

existing outstanding borrowings of $46.0 million. During the year ended December 31, 2009 and through September 2010 when we repaid our

borrowings under the prior credit facility, the weighted average interest rate for outstanding borrowings under the prior credit facility was

6.0%.

In September 2010, we entered into a new credit facility with a syndicate of banks with SunTrust Bank as administrative agent. The new

credit facility provides a $135.0 million revolving credit facility with the ability to request increases to the revolving credit facility of up to

$50.0 million. The initial borrowings under this new credit facility of $58.5 million were used to repay in full the outstanding indebtedness

under our prior credit facility and $1.5 million of debt issuance costs associated with the new credit facility. The new credit facility has a

maturity date in September 2015, and provides for and includes a $5.0 million swingline facility and $15.0 million letter of credit facility. At

our option, we may prepay any borrowings in whole or in part, without any prepayment penalty or premium.

As of December 31, 2010, we owed $58.5 million in outstanding borrowings under the new credit facility. During the year ended

December 31, 2010, the weighted average interest rate applicable to the outstanding borrowings on our new credit facility was 2.9%.

The new credit agreement contains certain financial and non-

financial covenants and requirements, including a leverage ratio, fixed charge

ratio and certain restrictions on our ability to make investments, pay dividends or sell assets. It also provides for customary events of default as

defined in the agreement, including failure to pay any principal or interest when due, failure to comply with covenants, and default in the event

of a change of control. We were in compliance with these covenants as of December 31, 2010.

In May 2009, we entered into a capital lease arrangement with a software provider for perpetual database licenses. The capital lease

arrangement resulted in the recognition of a $3.4 million capital lease liability, which was the present value of future payments under the lease

agreement discounted using an effective interest rate of 6.0%. As of December 31, 2010, approximately $1.4 million in principal payments

remained payable on the capital lease.

Off-Balance Sheet Arrangements

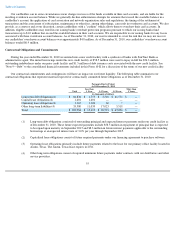

Our off-balance sheet arrangements are comprised of settlement indemnifications and overdraft guarantees with our issuing banks. We

have no off-balance sheet debt, other than operating leases, purchase orders, and other commitments entered into in the ordinary course of

business as discussed below and reflected in our contractual obligations and commitments table.

A significant portion of our business is conducted through our retail distributors that provide load and reload services to our cardholders at

their retail locations. Members of our distribution and reload network collect our cardholders' funds and remit them by electronic transfer

directly to our issuing banks for deposit in the cardholder accounts. We do not take possession of our cardholders' funds at any time during the

settlement process. Our issuing banks typically receive our cardholders' funds no earlier than three business days after they are collected by the

retailer. If any retailer fails to remit our cardholders' funds to our issuing banks, we typically reimburse our issuing banks for such funds. We

manage the settlement risk associated with this process through a formalized set of credit standards, limiting load volumes for certain retailers

and requiring certain retailers to maintain deposits on account, and by typically maintaining a right of offset of cardholders' funds against

commissions payable to retailers. As of December 31, 2010, our estimated gross settlement exposure was $13.9 million.

54