NetSpend 2010 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2010 NetSpend annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

|

|

Table of Contents

Recent Developments

Issuing Bank Diversification

We are pursuing a bank diversification strategy pursuant to which we intend to diversify our cards among at least three issuing banks. We

are focused on doing so in a manner that balances our diversification strategy with the protection of existing cardholder and direct deposit

relationships and other operational considerations. In furtherance of this strategy, in January 2011 we entered into an agreement with The

Bancorp Bank pursuant to which The Bancorp Bank will serve as a new issuing bank for our new and existing card programs. We expect to

begin marketing cards issued by The Bancorp Bank in April 2011. We have also continued our discussions with other prospective issuing

banks.

Interchange Legislation

We earn interchange revenues from a portion of the interchange fees remitted by merchants when cardholders make purchase transactions

using our prepaid debit cards. Interchange revenues are recognized net of sponsorship, licensing and processing fees charged by the card

associations and network organizations for services they provide in processing purchase transactions routed through their networks.

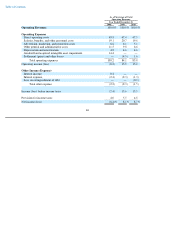

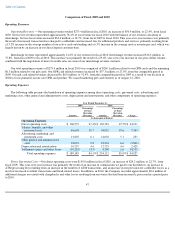

Interchange revenue represented approximately 17.0%, 19.2% and 21.6% of our revenues during the years ended December 31, 2008, 2009 and

2010, respectively. The amounts of these interchange fees are currently fixed by the card associations and network organizations in their sole

discretion.

In July 2010, the U.S. Congress adopted legislation that requires the amount of interchange fees charged to merchants in connection with

transactions utilizing traditional debit cards and certain prepaid cards issued by financial institutions that, together with their affiliates, have

assets of $10 billion or more, to be reasonable and proportionate to the costs of the underlying transactions. The new legislation also generally

gave the Federal Reserve Board the power to regulate the amount of such interchange fees and required the Federal Reserve Board to

promulgate regulations establishing standards for determining when interchange fees are reasonable and proportionate to the costs of the

underlying transactions. The Federal Reserve Board published proposed regulations in December 2010. The final regulations are scheduled to

be published in April 2011 and become effective in July 2011.

The proposed regulations prescribe limits on interchange fees that are below the current rates set by the card associations and network

organizations. Depending on the manner in which the limitations are clarified in the final regulations, these limitations may in the future limit

our ability to benefit from interchange regulation exemptions for GPR cards, or decrease the opportunity to earn additional revenue from

overdraft or ATM fees we might otherwise elect to charge. We currently believe that our GPR cards will be exempt from the regulations as

they stand currently. However, even if some or all of our GPR cards were exempt from any such interchange fee restrictions, it is possible that

such an exemption may be difficult to preserve if the relevant card associations or network organizations do not provide any mechanism that

enables the recognition of the exemption in processing transactions, which could result in a material adverse impact on our revenues. At the

present time, we do not believe that the proposed regulations will materially adversely impact our revenues, but we will continue to assess the

expected impact as the proposed regulations become finalized.

Treasury Department Rule

In January 2011, the Department of the Treasury issued an interim final rule that would prohibit the electronic deposit of federal benefits,

wages and tax refunds to prepaid debit cards that do not meet certain criteria, including that the card not have an attached line of credit or loan

feature that triggers automatic repayment from the card. The cardholder must also be afforded all of the consumer protections that apply to a

payroll card. The public comment period for the rule expires in April 2011.

42