Motorola 2009 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2009 Motorola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

64 MANAGEMENT’S DISCUSSION AND ANALYSIS

OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Inventory Valuation

The Company records valuation reserves on its inventory for estimated excess or obsolescence. The amount

of the reserve is equal to the difference between the cost of the inventory and the estimated market value based

upon assumptions about future demand and market conditions. On a quarterly basis, management in each

segment performs an analysis of the underlying inventory to identify reserves needed for excess and obsolescence.

Management uses its best judgment to estimate appropriate reserves based on this analysis. In addition, the

Company adjusts the carrying value of inventory if the current market value of that inventory is below its cost.

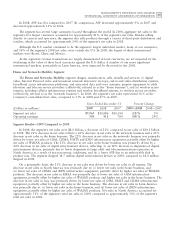

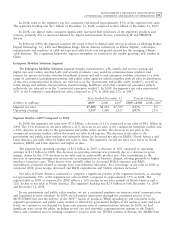

At December 31, 2009 and 2008, Inventories consisted of the following:

December 31 2009 2008

Finished goods $1,062 $1,710

Work-in-process and production materials 1,062 1,709

2,124 3,419

Less inventory reserves (816) (760)

$1,308 $2,659

The Company balances the need to maintain strategic inventory levels to ensure competitive delivery

performance to its customers against the risk of inventory obsolescence due to rapidly changing technology and

customer requirements. As reflected above, the Company’s inventory reserves represented 38% of the gross

inventory balance at December 31, 2009, compared to 22% of the gross inventory balance at December 31,

2008. The Company has inventory reserves for excess inventory, pending cancellations of product lines due to

technology changes, long-life cycle products, lifetime buys at the end of supplier production runs, business exits,

and a shift of production to outsourcing.

If future demand or market conditions are less favorable than those projected by management, additional

inventory writedowns may be required.

Income Taxes

The Company’s effective tax rate is based on pre-tax income and the tax rates applicable to that income in

the various jurisdictions in which the Company operates. An estimated effective tax rate for a year is applied to

the Company’s quarterly operating results. In the event that there is a significant unusual or discrete item

recognized, or expected to be recognized, in the Company’s quarterly operating results, the tax attributable to

that item would be separately calculated and recorded at the same time as the unusual or discrete item. The

Company considers the resolution of prior-year tax matters to be such items. Significant judgment is required in

determining the Company’s effective tax rate and in evaluating its tax positions. The Company establishes

reserves when it is more likely than not that the Company will not realize the full tax benefit of the position. The

Company adjusts these reserves in light of changing facts and circumstances.

Tax regulations may require items of income and expense to be included in a tax return in different periods

than the items are reflected in the consolidated financial statements. As a result, the effective tax rate reflected in

the consolidated financial statements may be different than the tax rate reported in the income tax return. Some

of these differences are permanent, such as expenses that are not deductible on the tax return, and some are

temporary differences, such as depreciation expense. Temporary differences create deferred tax assets and

liabilities. Deferred tax assets generally represent items that can be used as a tax deduction or credit in the tax

return in future years for which the Company has already recorded the tax benefit in the consolidated financial

statements. Deferred tax liabilities generally represent tax expense recognized in the consolidated financial

statements for which payment has been deferred or expense for which the Company has already taken a

deduction on an income tax return, but has not yet recognized in the consolidated financial statements.

The Company accounts for income taxes by recognizing deferred tax assets and liabilities using enacted tax

rates for the effect of the temporary differences between the book and tax basis of recorded assets and liabilities.

The Company makes estimates and judgments with regard to the calculation of certain income tax assets and

liabilities. Deferred tax assets are reduced by valuation allowances if, based on the consideration of all available

evidence, it is more likely than not that some portion of the deferred tax asset will not be realized. Significant

weight is given to evidence that can be objectively verified.