Motorola 2009 Annual Report Download - page 112

Download and view the complete annual report

Please find page 112 of the 2009 Motorola annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

104

The Company uses a five-year, market-related asset value method of amortizing asset-related gains and losses.

Prior service costs are being amortized over periods ranging from 11 to 12 years. Benefits under all pension plans

are valued based upon the projected unit credit cost method.

Certain actuarial assumptions such as the discount rate and the long-term rate of return on plan assets have

a significant effect on the amounts reported for net periodic cost and benefit obligation. The assumed discount

rates reflect the prevailing market rates of a universe of high-quality, non-callable, corporate bonds currently

available that, if the obligation were settled at the measurement date, would provide the necessary future cash

flows to pay the benefit obligation when due. The long-term rates of return on plan assets represents an estimate

of long-term returns on an investment portfolio consisting of a mixture of equities, fixed income, cash and other

investments similar to the actual investment mix. In determining the long-term return on plan assets, the

Company considers long-term rates of return on the asset classes (both historical and forecasted) in which the

Company expects the plan funds to be invested.

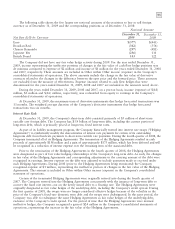

Weighted average actuarial assumptions used to determine costs for the plans were as follows:

2009 2008

December 31 U.S. Non U.S. U.S. Non U.S.

Discount rate 6.75% 6.23% 6.75% 5.73%

Investment return assumption (Regular Plan) 8.25% 6.86% 8.50% 6.55%

Investment return assumption (Officers’ Plan) 6.00% N/A 6.00% N/A

Weighted average actuarial assumptions used to determine benefit obligations for the plans were as follows:

2009 2008

December 31 U.S. Non U.S. U.S. Non U.S.

Discount rate 6.00% 5.46% 6.75% 6.16%

Future compensation increase rate (Regular Plan) 0.00% 4.28% 0.00% 4.24%

Future compensation increase rate (Officers’ Plan) 0.00% N/A 0.00% N/A

The accumulated benefit obligations for the plans were as follows:

2009 2008

Officers’ Officers’

and Non and Non

December 31 Regular MSPP U.S. Regular MSPP U.S.

Accumulated benefit obligation $5,821 $52 $1,527 $5,110 $116 $1,163

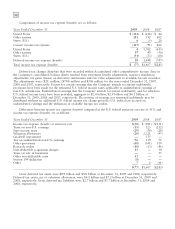

The Company has adopted a pension investment policy designed to meet or exceed the expected rate of

return on plan assets assumption. To achieve this, the pension plans retain professional investment managers that

invest plan assets in equity and fixed income securities and cash. In addition, some plans invest in insurance

contracts. The Company’s measurement date of its plan assets and obligations is December 31. The Company has

the following target mixes for these asset classes, which are readjusted periodically, when an asset class weighting

deviates from the target mix, with the goal of achieving the required return at a reasonable risk level:

Target Mix

Asset Category 2009 2008

Equity securities 63% 71%

Fixed income securities 35% 27%

Cash and other investments 2% 2%