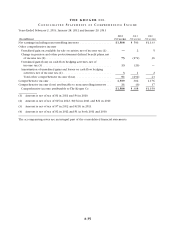

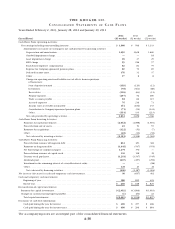

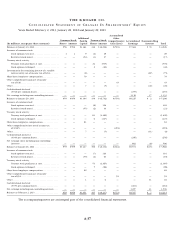

Kroger 2012 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2012 Kroger annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

A-41

NO T E S T O C O N S O L I D A T E D F I N A N C I A L S T A T E M E N T S , CO N T I N U E D

Benefit Plans and Multi-Employer Pension Plans

The Company recognizes the funded status of its retirement plans on the Consolidated Balance Sheet.

Actuarial gains or losses, prior service costs or credits and transition obligations that have not yet been

recognized as part of net periodic benefit cost are required to be recorded as a component of Accumulated

Other Comprehensive Income (“AOCI”). All plans are measured as of the Company’s fiscal year end.

The determination of the obligation and expense for Company-sponsored pension plans and other

post-retirement benefits is dependent on the selection of assumptions used by actuaries and the Company

in calculating those amounts. Those assumptions are described in Note 13 and include, among others, the

discount rate, the expected long-term rate of return on plan assets and the rates of increase in compensation

and health care costs. Actual results that differ from the assumptions are accumulated and amortized over

future periods and, therefore, generally affect the recognized expense and recorded obligation in future

periods. While the Company believes that the assumptions are appropriate, significant differences in actual

experience or significant changes in assumptions may materially affect the pension and other post-retirement

obligations and future expense.

The Company also participates in various multi-employer plans for substantially all union employees.

Pension expense for these plans is recognized as contributions are funded. Refer to Note 14 for additional

information regarding the Company’s participation in these various multi-employer plans and the United Food

and Commercial Workers International Union (“UFCW”) consolidated fund.

The Company administers and makes contributions to the employee 401(k) retirement savings accounts.

Contributions to the employee 401(k) retirement savings accounts are expensed when contributed. Refer to

Note 13 for additional information regarding the Company’s benefit plans.

Stock Based Compensation

The Company accounts for stock options under fair value recognition provisions. Under this method, the

Company recognizes compensation expense for all share-based payments granted. The Company recognizes

share-based compensation expense, net of an estimated forfeiture rate, over the requisite service period of

the award. In addition, the Company records expense for restricted stock awards in an amount equal to the

fair market value of the underlying stock on the grant date of the award, over the period the awards lapse.

Deferred Income Taxes

Deferred income taxes are recorded to reflect the tax consequences of differences between the tax basis

of assets and liabilities and their financial reporting basis. Refer to Note 4 for the types of differences that give

rise to significant portions of deferred income tax assets and liabilities. Deferred income taxes are classified

as a net current or noncurrent asset or liability based on the classification of the related asset or liability for

financial reporting purposes. A deferred tax asset or liability that is not related to an asset or liability for

financial reporting is classified according to the expected reversal date.

Uncertain Tax Positions

The Company reviews the tax positions taken or expected to be taken on tax returns to determine

whether and to what extent a benefit can be recognized in its consolidated financial statements. Refer to Note 4

for the amount of unrecognized tax benefits and other related disclosures related to uncertain tax positions.

Various taxing authorities periodically audit the Company’s income tax returns. These audits include

questions regarding the Company’s tax filing positions, including the timing and amount of deductions and

the allocation of income to various tax jurisdictions. In evaluating the exposures connected with these various

tax filing positions, including state and local taxes, the Company records allowances for probable exposures. A

number of years may elapse before a particular matter, for which an allowance has been established, is audited

and fully resolved. As of February 2, 2013, the Internal Revenue Service had concluded its field examination