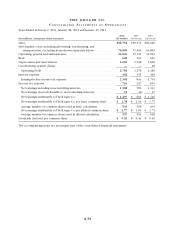

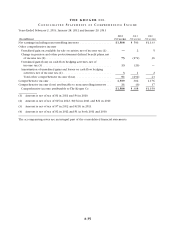

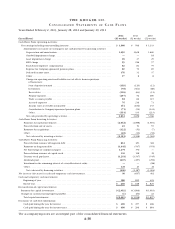

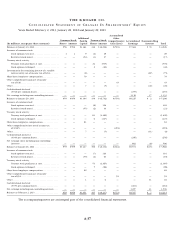

Kroger 2012 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 2012 Kroger annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

A-27

Statements elsewhere in this report and below regarding our expectations, projections, beliefs, intentions

or strategies are forward-looking statements within the meaning of Section 21E of the Securities Exchange

Act of 1934. While we believe that the statements are accurate, uncertainties about the general economy, our

labor relations, our ability to execute our plans on a timely basis and other uncertainties described below

could cause actual results to differ materially.

• Weexpectnetearningsperdilutedshareintherangeof$2.71-$2.79for2013.Thisequatestoourlong-

term growth rate of 8% to 11% from our adjusted fiscal 2012 net earnings per diluted share of $2.52,

which excludes the UFCW consolidated pension accrual and credit card settlement adjustments in the

third quarter of 2012 and the extra week in the fourth quarter of 2012. We expect the first quarter

net earnings per diluted share growth rate for 2013 to be on the low end of the range primarily due to

expected inflation being lower in the first quarter of 2013, compared to 2012, and the growth of our

pharmacy business not being as substantial as in the first quarter of 2012. We expect the second and

third quarters net earnings per diluted share growth rate for 2013 to be at the high end to above the

range primarily due to expected inflation being more comparable in the second and third quarters of

2013, compared to the second and third quarters of 2012, and expecting our identical supermarket sales

to be trending upwards. We also expect the fourth quarter net earnings per diluted share growth rate

for 2013 to be lower than the prior year on a 12-week to 12-week basis primarily due to a budgeted LIFO

charge of $13 million compared to a LIFO credit of $41 million in the fourth quarter of 2012.

• Weexpectidenticalsupermarketsalesgrowth,excludingfuelsales,of2.5%-3.5%in2013.Weexpect

identical supermarket sales growth to increase over time during 2013 relative to 2012. In 2012, we

experienced higher levels of inflation early in the year. In the second half of the year, several branded

prescription drugs came off patent, and when branded prescription drugs come off patent and are sold

as generics, sales are reduced because generic equivalents have lower retail prices than branded drugs.

We do not expect these conditions to continue to have the same impact for 2013.

• Ourlong-termbusinessmodel seekstoproduce annualearningsperdiluted sharegrowthaveraging

8.0%-11.0%, plus a dividend of 2.0% to 2.5%, for a total shareholder return of approximately 10.0%-13.5%.

• For2013,weintendtocontinuetofocusonimprovingsalesgrowth,inaccordancewithourCustomer

1st strategy, by making investments in gross margin and customer shopping experiences. We expect to

finance these investments primarily with operating cost reductions. We expect FIFO non-fuel operating

margins for 2013 to expand slightly compared to 2012, excluding the UFCW consolidated pension plan

accrual and the credit card settlement adjustments in 2012.

• For2013,weexpectourannualizedLIFOchargetobeapproximately$55million.Thisforecastisbased

on estimated cost changes for products in our inventory.

• For 2013, we expect interest expense to be approximately $440 million.

• We plan to use cash flow primarily for capital investments, to maintain our current debt coverage ratios,

to pay cash dividends, and to repurchase stock. As market conditions change, we may re-evaluate these

uses of cash flow.

• We expect to obtain sales growth from new square footage, as well as from increased productivity from

existing locations.

• Capitalinvestmentsreflectourstrategyofgrowththroughexpansion,fillingintargetedexistingmarkets,

entering a new market and focusing on productivity increases from our existing store base through

remodels. In addition, we intend to continue our emphasis on self-development and ownership of real

estate, and logistics and technology improvements. Our continued capital spending on technology is

focused on improving store operations, logistics, manufacturing procurement, category management,

merchandising and buying practices, and is expected to reduce merchandising costs. We intend to

continue using cash flow from operations to finance capital expenditure requirements. We expect capital

investments for 2013 to increase to the range of $2.1-$2.4 billion, excluding acquisitions and purchases

of leased facilities. We also expect capital investments to increase incrementally $200 million over the