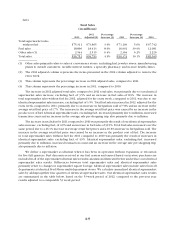

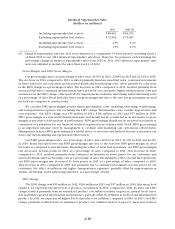

Kroger 2012 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2012 Kroger annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

A-17

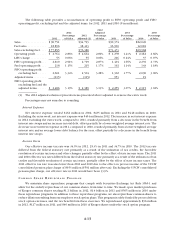

The annual evaluation of goodwill performed during the fourth quarter of 2012 and 2011 did not result

in impairment.

The annual evaluation of goodwill performed during the fourth quarter of 2010 resulted in an impairment

charge of $18 million. Based on the results of our step one analysis in the fourth quarter of 2010, a supermarket

reporting unit with a small number of stores indicated potential impairment. Due to estimated future expected

cash flows being lower than in the past, our estimated fair value of the reporting unit decreased. We concluded

that the carrying value of goodwill for this reporting unit exceeded its implied fair value, resulting in a pre-

tax impairment charge of $18 million ($12 million after-tax). In 2009, we disclosed that a 10% reduction in

fair value of this supermarket reporting unit would indicate a potential for impairment. Subsequent to the

impairment, no goodwill remains at this reporting unit.

Based on current and future expected cash flows, we believe goodwill impairments are not reasonably

possible. A 10% reduction in fair value of our reporting units would not indicate a potential for impairment of

our goodwill balance.

For additional information relating to our results of the goodwill impairment reviews performed

during 2012, 2011 and 2010 see Note 2 to the Consolidated Financial Statements.

The impairment review requires the extensive use of management judgment and financial estimates.

Application of alternative estimates and assumptions, such as reviewing goodwill for impairment at a different

level, could produce significantly different results. The cash flow projections embedded in our goodwill

impairment reviews can be affected by several factors such as inflation, business valuations in the market, the

economy and market competition.

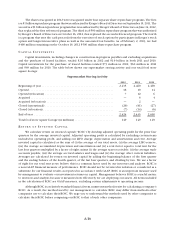

Store Closing Costs

We provide for closed store liabilities on the basis of the present value of the estimated remaining non-

cancellable lease payments after the closing date, net of estimated subtenant income. We estimate the net lease

liabilities using a discount rate to calculate the present value of the remaining net rent payments on closed

stores. We usually pay closed store lease liabilities over the lease terms associated with the closed stores,

which generally have remaining terms ranging from one to 20 years. Adjustments to closed store liabilities

primarily relate to changes in subtenant income and actual exit costs differing from original estimates. We

make adjustments for changes in estimates in the period in which the change becomes known. We review store

closing liabilities quarterly to ensure that any accrued amount that is not a sufficient estimate of future costs,

or that no longer is needed for its originally intended purpose, is adjusted to earnings in the proper period.

We estimate subtenant income, future cash flows and asset recovery values based on our experience and

knowledge of the market in which the closed store is located, our previous efforts to dispose of similar assets

and current economic conditions. The ultimate cost of the disposition of the leases and the related assets is

affected by current real estate markets, inflation rates and general economic conditions.

We reduce owned stores held for disposal to their estimated net realizable value. We account for costs to

reduce the carrying values of property, equipment and leasehold improvements in accordance with our policy

on impairment of long-lived assets. We classify inventory write-downs in connection with store closings, if

any, in “Merchandise costs.” We expense costs to transfer inventory and equipment from closed stores as they

are incurred.

Post-Retirement Benefit Plans

We account for our defined benefit pension plans using the recognition and disclosure provisions of

GAAP, which require the recognition of the funded status of retirement plans on the Consolidated Balance

Sheet. We record, as a component of Accumulated Other Comprehensive Income (“AOCI”), actuarial gains or

losses, prior service costs or credits and transition obligations that have not yet been recognized.

The determination of our obligation and expense for Company-sponsored pension plans and other post-

retirement benefits is dependent upon our selection of assumptions used by actuaries in calculating those

amounts. Those assumptions are described in Note 13 to the Consolidated Financial Statements and include,