Kroger 2012 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2012 Kroger annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

A-18

among others, the discount rate, the expected long-term rate of return on plan assets, average life expectancy

and the rate of increases in compensation and health care costs. Actual results that differ from our assumptions

are accumulated and amortized over future periods and, therefore, generally affect our recognized expense

and recorded obligation in future periods. While we believe that our assumptions are appropriate, significant

differences in our actual experience or significant changes in our assumptions, including the discount rate

used and the expected return on plan assets, may materially affect our pension and other post-retirement

obligations and our future expense. Note 13 to the Consolidated Financial Statements discusses the effect

of a 1% change in the assumed health care cost trend rate on other post-retirement benefit costs and the

related liability.

The objective of our discount rate assumptions was intended to reflect the rates at which the pension

benefits could be effectively settled. In making this determination, we take into account the timing and

amount of benefits that would be available under the plans. Our policy for selecting the discount rates as of

year-end 2012 changed from the policy as of year-end 2011 and 2010. In 2012, our policy was to match the

plan’s cash flows to that of a hypothetical bond portfolio whose cash flow from coupons and maturities match

the plan’s projected benefit cash flows. The discount rates are the single rates that produce the same present

value of cash flows. The selection of the 4.29% and 4.11% discount rates as of year-end 2012 for pension and

other benefits, respectively, represents the hypothetical bond portfolio using bonds with an AA or better

rating constructed with the assistance of an outside consultant. In 2011 and 2010, our policy was to match the

plan’s cash flows to that of a yield curve that provides the equivalent yields on zero-coupon corporate bonds

for each maturity. Benefit cash flows due in a particular year can theoretically be “settled” by “investing” them

in the zero-coupon bond that matures in the same year. The discount rates are the single rates that produce

the same present value of cash flows. The selection of the 4.55% and 4.40% discount rates as of year-end

2011 for pension and other benefits, respectively, represents the equivalent single rates constructed under

a broad-market AA yield curve constructed with the assistance of an outside consultant. A 100 basis point

increase in the discount rate would decrease the projected pension benefit obligation as of February 2, 2013,

by approximately $412.

To determine the expected rate of return on pension plan assets, we consider current and forecasted

plan asset allocations as well as historical and forecasted rates of return on various asset categories. For 2012

and 2011, we assumed a pension plan investment return rate of 8.5%. Our pension plan’s average rate of

return was 9.7% for the 10 calendar years ended December 31, 2012, net of all investment management fees

and expenses. The value of all investments in our Company-sponsored defined benefit pension plans during

the calendar year ending December 31, 2012, net of investment management fees and expenses, increased

15.0%. For the past 20 years, our average annual rate of return has been 9.9%. The average annual return for

the S&P 500 over the same period of time has been 8.5%. Based on the above information and forward looking

assumptions for investments made in a manner consistent with our target allocations, we believe an 8.5% rate

of return assumption is reasonable. See Note 13 to the Consolidated Financial Statements for more information

on the asset allocations of pension plan assets.

Sensitivity to changes in the major assumptions used in the calculation of Kroger’s pension plan liabilities

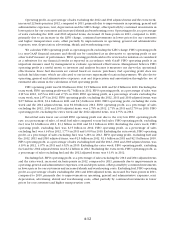

for the qualified plans is illustrated below (in millions).

Percentage

Point Change

Projected Benefit

Obligation

Decrease/(Increase)

Expense

Decrease/(Increase)

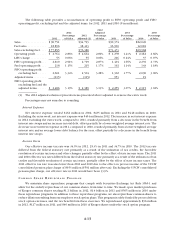

Discount Rate.............................. +/- 1.0% $412/(502) $32/($36)

Expected Return on Assets ................... +/- 1.0% — $26/($26)

We contributed $71 million in 2012, $52 million in 2011 and $141 million in 2010 to our Company-

sponsored defined benefit pension plans. In February 2013, we contributed $100 million to the Company-

sponsored defined benefit pension plans and do not expect to make any additional contributions in 2013. We

expect contributions made during 2013 will decrease our required contributions in future years. Among other

things, investment performance of plan assets, the interest rates required to be used to calculate the pension

obligations, and future changes in legislation, will determine the amounts of contributions.