Kraft 2004 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2004 Kraft annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

|

|

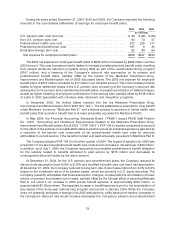

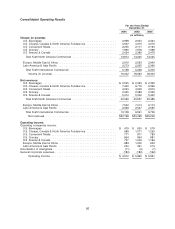

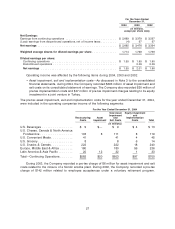

During the years ended December 31, 2004, 2003 and 2002, the Company recorded the following

amounts in the consolidated statements of earnings for employee benefit plans:

2004 2003 2002

(in millions)

U.S. pension plan cost (income) ................................. $ 46 $(46) $(33)

Non-U.S. pension plan cost ..................................... 93 74 47

Postretirement health care cost .................................. 237 229 217

Postemployment benefit plan cost ................................ 167 6 35

Employee savings plan cost .................................... 92 84 64

Net expense for employee benefit plans .......................... $635 $347 $330

The 2004 net expense for employee benefit plans of $635 million increased by $288 million over the

2003 amount. This cost increase primarily relates to increased postemployment benefit costs, resulting

from several workforce reduction programs during 2004 as part of the overall restructuring program

($167 million), and a lowering of the Company’s discount rate assumption on its pension and

postretirement benefit plans, partially offset by the impact of the Medicare Prescription Drug,

Improvement and Modernization Act of 2003 discussed below. The 2003 net expense for employee

benefit plans of $347 million increased by $17 million over the 2002 amount. This cost increase primarily

relates to higher settlement losses in the U.S. pension plan, a lowering of the Company’s discount rate

assumption on its pension and postretirement benefit plans, increased amortization of deferred losses,

as well as higher matching of employee contributions in the savings plan, partially offset by $148 million

of costs in 2002 associated with voluntary early retirement and integration programs.

In December 2003, the United States enacted into law the Medicare Prescription Drug,

Improvement and Modernization Act of 2003 (the ‘‘Act’’). The Act establishes a prescription drug benefit

under Medicare, known as ‘‘Medicare Part D,’’ and a federal subsidy to sponsors of retiree health care

benefit plans that provide a benefit that is at least actuarially equivalent to Medicare Part D.

In May 2004, the Financial Accounting Standards Board (‘‘FASB’’) issued FASB Staff Position

No. 106-2, ‘‘Accounting and Disclosure Requirements Related to the Medicare Prescription Drug,

Improvement and Modernization Act of 2003’’ (‘‘FSP 106-2’’). FSP 106-2 requires companies to account

for the effect of the subsidy on benefits attributable to past service as an actuarial experience gain and as

a reduction of the service cost component of net postretirement health care costs for amounts

attributable to current service, if the benefit provided is at least actuarially equivalent to Medicare Part D.

The Company adopted FSP 106-2 in the third quarter of 2004. The impact of adoption for 2004 was

a reduction of pre-tax net postretirement health care costs and an increase in net earnings of $24 million.

In addition, as of July 1, 2004, the Company reduced its accumulated postretirement benefit obligation

for the subsidy related to benefits attributed to past service by $315 million and decreased its

unrecognized actuarial losses by the same amount.

At December 31, 2004, for the U.S. pension and postretirement plans, the Company reduced its

discount rate assumption from 6.25% to 5.75% and modified its health care cost trend rate assumption.

At December 31, 2004, the Company reduced its long-term rate of return assumption from 9.0% to 8.0%

based on the investment return of its pension assets, which are primarily in U.S. equity securities. The

Company presently anticipates that these assumption changes, coupled with the amortization of lower

returns on pension fund assets in prior years, partially offset by the full year effect of adopting Medicare

Part D, will result in an increase in 2005 pre-tax benefit expense of approximately $200 million, or

approximately $0.08 per share. The expected increase in benefit expense is prior to the consideration of

any impact of the three-year restructuring program announced in January 2004. While the Company

does not presently anticipate a change in its 2005 assumptions, a fifty-basis point decline (increase) in

the Company’s discount rate would increase (decrease) the Company’s pension and postretirement

19