Honeywell 2009 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2009 Honeywell annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

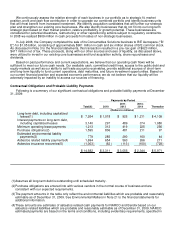

|

|

•

significant changes or planned changes in our use of the assets.

Once it is determined that an impairment review is necessary, recoverability of assets is measured by

comparing the carrying amount of the asset grouping to the estimated future undiscounted cash flows. If the

carrying amount exceeds the estimated future undiscounted cash flows, the asset grouping is considered to be

impaired. The impairment is then measured as the difference between the carrying amount of the asset grouping

and its fair value. We endeavor to utilize the best information available to measure fair value, which is usually

either market prices (if available), level 1 or level 2 in the fair value hierarchy or an estimate of the future

discounted cash flow, level 3 of the fair value hierarchy. The key estimates in our discounted cash flow analysis

include expected industry growth rates, our assumptions as to volume, selling prices and costs, and the discount

rate selected. As described in more detail in Note 16 to the financial statements, we have recorded impairment

charges related to long-lived assets of $28 and $78 million in 2009 and 2008, respectively, principally related to

manufacturing plant and equipment in facilities scheduled to close or be downsized.

Goodwill Impairment Testing—Goodwill represents the excess of acquisition costs over the fair value of

the net tangible assets and identifiable intangible assets acquired in a business combination. Goodwill is not

amortized, but is subject to impairment testing. Our Goodwill balance, $10.5 billion as of December 31, 2009, is

subject to impairment testing annually as of March 31, or whenever events or changes in circumstances indicate

that the carrying amount may not be fully recoverable. This testing compares carrying values to fair values and,

when appropriate, the carrying value is reduced to fair value. The fair value of our reporting units is estimated

utilizing a discounted cash flow approach utilizing cash flow forecasts in our five year strategic and annual

operating plans adjusted for terminal value assumptions. This impairment test involves the use of accounting

estimates and assumptions, changes in which could materially impact our financial condition or operating

performance if actual results differ from such estimates and assumptions. To address this uncertainty we perform

sensitivity analysis on key estimates and assumptions.

We completed our annual impairment test as of March 31, 2009 and determined that there was no

impairment as of that date. Given the significant changes in the business climate and decline in mid-range

forecasts for certain of our reporting units we re-tested goodwill for impairment in the second half of 2009. No

impairment was indicated by this interim test. However, significant negative industry or economic trends,

disruptions to our business, unexpected significant changes or planned changes in use of the assets, divestitures

and market capitalization declines may have a negative effect on the fair value of our reporting units.

Income Taxes—Deferred tax assets and liabilities are determined based on the difference between the

financial statements and tax basis of assets and liabilities using enacted tax rates in effect for the year in which

the differences are expected to reverse. Our provision for income taxes is based on domestic and international

statutory income tax rates in the jurisdictions in which we operate. Significant judgment is required in determining

income tax provisions as well as deferred tax asset and liability balances, including the estimation of valuation

allowances and the evaluation of tax positions.

As of December 31, 2009, we recognized a net deferred tax asset of $3,028 million, less a valuation

allowance of $578 million. Net deferred tax assets are primarily comprised of net deductible temporary

differences, net operating loss carryforwards and tax credit carryforwards that are available to reduce taxable

income in future periods. The determination of the amount of valuation allowance to be provided on recorded

deferred tax assets involves estimates regarding (1) the timing and amount of the reversal of taxable temporary

differences, (2) expected future taxable income, and (3) the impact of tax planning strategies. A valuation

allowance is established to offset any deferred tax assets if, based upon the available evidence it is more likely

than not that some or all of the deferred tax asset will not be realized. In assessing the need for a valuation

allowance, we consider all available positive and negative evidence, including past operating results, projections

of future taxable income and the feasibility of ongoing tax planning strategies. The projections of future taxable

income include a number of estimates and assumptions regarding our volume, pricing and costs. Additionally,

valuation allowances related to deferred tax assets can be impacted by changes to tax laws.

Our net deferred tax asset of $3,028 million is comprised of $2,132 million related to U.S. operations and

$896 million related to non-U.S. operations. The U.S. net deferred tax asset of $2,132

47