Honeywell 2009 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2009 Honeywell annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

|

|

not use derivative financial instruments for trading or other speculative purposes and do not use leveraged

derivative financial instruments. A summary of our accounting policies for derivative financial instruments is

included in Note 1 to the financial statements. We also hold investments in marketable equity securities, which

exposes us to market volatility, as discussed in Note 16 to the financial statements.

We conduct our business on a multinational basis in a wide variety of foreign currencies. Our exposure to

market risk from changes in foreign currency exchange rates arises from international financing activities

between subsidiaries, foreign currency denominated monetary assets and liabilities and anticipated transactions

arising from international trade. Our objective is to preserve the economic value of non-functional currency cash

flows. We attempt to hedge transaction exposures with natural offsets to the fullest extent possible and, once

these opportunities have been exhausted, through foreign currency forward and option agreements with third

parties. Our principal currency exposures relate to the U.S. dollar, Euro, British pound, Canadian dollar, Hong

Kong dollar, Mexican peso, Swiss franc, Czech koruna, Chinese renminbi, Indian rupee, and Singapore dollar.

Our exposure to market risk from changes in interest rates relates primarily to our net debt and pension

obligations. As described in Notes 14 and 16 to the financial statements, we issue both fixed and variable rate

debt and use interest rate swaps to manage our exposure to interest rate movements and reduce overall

borrowing costs.

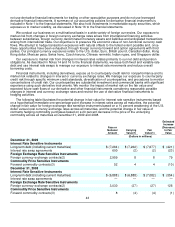

Financial instruments, including derivatives, expose us to counterparty credit risk for nonperformance and to

market risk related to changes in interest or currency exchange rates. We manage our exposure to counterparty

credit risk through specific minimum credit standards, diversification of counterparties, and procedures to monitor

concentrations of credit risk. Our counterparties are substantial investment and commercial banks with significant

experience using such derivative instruments. We monitor the impact of market risk on the fair value and

expected future cash flows of our derivative and other financial instruments considering reasonably possible

changes in interest and currency exchange rates and restrict the use of derivative financial instruments to

hedging activities.

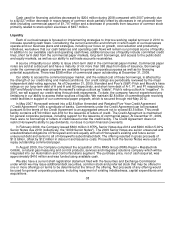

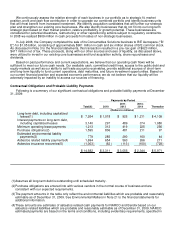

The following table illustrates the potential change in fair value for interest rate sensitive instruments based

on a hypothetical immediate one-percentage-point increase in interest rates across all maturities, the potential

change in fair value for foreign exchange rate sensitive instruments based on a 10 percent weakening of the U.S.

dollar versus local currency exchange rates across all maturities, and the potential change in fair value of

contracts hedging commodity purchases based on a 20 percent decrease in the price of the underlying

commodity across all maturities at December 31, 2009 and 2008.

Face or

Notional

Amount Carrying

Value(1) Fair

Value(1)

Estimated

Increase

(Decrease)

In Fair

Value

(Dollars in millions)

December 31, 2009

Interest Rate Sensitive Instruments

Long-term debt (including current maturities) $ (7,264) $ (7,262) $ (7,677) $ (421)

Interest rate swap agreements 600 (2) (2) (23)

Foreign Exchange Rate Sensitive Instruments

Foreign currency exchange contracts(2) 2,959 8 8 79

Commodity Price Sensitive Instruments

Forward commodity contracts(3) 52 4 4 (10)

December 31, 2008

Interest Rate Sensitive Instruments

Long-term debt (including current maturities) $ (6,888) $ (6,888) $ (7,082) $ (354)

Interest rate swap agreements — — — —

Foreign Exchange Rate Sensitive Instruments

Foreign currency exchange contracts(2) 3,030 (27) (27) 126

Commodity Price Sensitive Instruments

Forward commodity contracts(3) 8 (4) (4) (1)

43