HTC 2009 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2009 HTC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

|

|

As a result, the carrying value of this investment became zero and the

Company reversed a capital surplus of NT$2,360 thousand (US$74 thousand)

that was recognized in prior years for the movement of Vitamin D’s capital

surplus in proportion to the Company’s equivalent stock. Also recognized

was the movement of other investees’ capital surplus amounting to

NT$2,566 thousand (US$80 thousand). As of December 31, 2009, the total

capital surplus from long-term equity-method investments was NT$18,411

thousand (US$576 thousand).

The additional paid-in capital from a merger was NT$25,756 thousand as of

January 1, 2008. Then because of treasury stock retirement in January and

November 2009, the additional paid-in capital from a merger decreased to

NT$25,189 thousand (US$787 thousand) as of December 31, 2009.

Appropriation of Retained Earnings and Dividend Policy

Based on the Company Law of the ROC and the Company’s Articles of

Incorporation, 10% of the Company’s annual net income less any deficit

should first be appropriated as legal reserve. From the remainder, there

should be appropriations of not more than 3‰ as remuneration to directors

and supervisors and at least 5% as bonuses to employees.

The appropriation of retained earnings should be proposed by the board of

directors and approved by the stockholders in their annual meeting.

As part of a high-technology industry and a growing enterprise, the Company

considers its operating environment, industry developments, and long-term

interests of stockholders as well as its programs to maintain operating

efficiency and meet its capital expenditure budget and financial goals in

determining the stock or cash dividends to be paid. The Company’s

dividend policy stipulates that at least 50% of total dividends may be

distributed as cash dividends.

Had the Company recognized the employees’ bonuses of NT$1,313,200

thousand as expenses in 2007, the pro forma earnings per share in 2007

would have decreased from NT$50.48 to NT$48.19, which were not adjusted

retroactively for the effect of stock dividend distribution in the following year.

The bonus to employees of NT$6,164,889 thousand for 2008 were approved

in the stockholders’ meeting in June 2009. The bonus to employees

included a cash bonus of NT$1,210,000 thousand and a share bonus of

NT$4,954,889 thousand. The number of shares of 13,357 thousand was

determined by dividing the amount of share bonus by the closing price (after

considering the effect of cash and stock dividends) of the shares of the day

immediately preceding the stockholders’ meeting. The approved amounts

of the bonus to employees were the same as the accrued amounts.

Based on a resolution passed by the Company’s board of directors in

February 2009, the employee bonus for 2009 should be appropriated at 18%

of net income before deducting employee bonus expenses. If the actual

amounts subsequently resolved by the stockholders differ from the proposed

amounts, the differences are recorded in the year of stockholders’ resolution

as a change in accounting estimate. If bonus shares are resolved to be

distributed to employees, the number of shares is determined by dividing the

amount of bonus by the closing price (after considering the effect of cash and

stock dividends) of the shares of the day immediately preceding the

stockholders’ meeting.

As of January 18, 2010, the date of the accompanying independent

auditors’ report, the appropriation of the 2009 earnings had not been

proposed by the Board of Directors. Information on earnings appropriation

can be accessed online through the Market Observation Post System on the

Web site.

)LQDQFLDO,QIRUPDWLRQ

Global Depositary Receipts

The Company issued 14,400 thousand common shares corresponding to

3,600 thousand units of Global Depositary Receipts (GDRs). For this GDR

issuance, the Company’s stockholders, including Via Technologies, Inc., also

issued 12,878.4 thousand common shares, corresponding to 3,219.6

thousand GDR units. Thus, the entire offering consisted of 6,819.6 thousand

GDR units. Each GDR represents four common shares, with par value of

NT$131.1. For this common share issuance, net of related expenses,

NT$1,696,855 thousand was accounted for as capital surplus. This share

issuance for cash was completed and registered on November 19, 2003.

The holders of these GDRs have the same rights and obligations as the

stockholders of the Company. However, the distribution of the offering and

sales of GDRs and the shares represented thereby in certain jurisdictions may

be restricted by law. In addition, the GDRs offered and the shares

represented are not transferable, except in accordance with the restrictions

described in the GDR offering circular and related laws applied in Taiwan.

Through the depositary custodian in Taiwan, GDR holders are entitled to

exercise these rights:

a. To vote; and

b. To receive dividends and participate in new share issuance for cash

subscription.

Taking into account the effect of stock dividends, the GDRs increased to

8,493 thousand units (33,971.9 thousand shares). The holders of these

GDRs requested the Company to redeem the GDRs to get the Company’s

common shares. As of December 31, 2009, there were 3,067.4 thousand

units of GDRs redeemed, representing 12,270 thousand common shares, and

the outstanding GDRs represented 21,702 thousand common shares or

2.75% of the Company’s common shares.

Capital Surplus

Under the Company Law, capital surplus can only be used to offset a deficit.

However, the capital surplus from share issued in excess of par (additional

paid-in capital from issuance of common shares, conversion of bonds and

treasury stock transactions) and donations may be capitalized, which

however is limited to a certain percentage of the Company’s paid-in capital.

Also, the capital surplus from long-term investments may not be used for any

purpose.

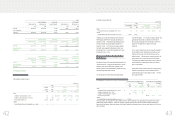

The additional paid-in capital was NT$4,374,244 thousand as of January 1,

2008. In January and November 2009, the retirement of treasury stock

caused a decrease of additional paid-in capital amounted to NT$57,907

thousand (US$1,810 thousand) and NT$81,330 thousand (US$2,542

thousand), respectively. In addition, the bonus to employees of

NT$6,164,889 thousand for 2008 were approved in the stockholders’

meeting in June 2009. Of the approved amount, NT$4,954,889 thousand,

representing 13,357 thousand common shares which was determined by fair

value, would be distributed by common stock. The difference between par

value and fair value of NT$4,821,316 thousand (US$150,713 thousand) was

accounted for as additional paid-in capital. As a result, the additional paid-in

capital as of December 31, 2009 was NT$9,056,323 thousand (US$283,099

thousand). Under the Company Law, the Company may transfer the capital

surplus to common stock if there is no accumulated deficit.

The capital surplus from long-term equity investments was NT$15,845

thousand as of January 1, 2008. When the Company did not subscribe for

the new shares issued by Vitamin D Inc. in September 2008, January 2009

and June 2009, adjustments of NT$1,689 thousand, NT$187 thousand (US$6

thousand) and NT$484 thousand (US$15 thousand) were made to the

investment carrying value and capital surplus, respectively. The Company

also determined that the recoverable amount of this investment was less than

its carrying amount and recognized an impairment loss on its carrying value.

)LQDQFLDO,QIRUPDWLRQ