HTC 2009 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2009 HTC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

|

|

6968

CORPORATE GOVERNANCE

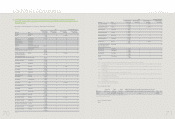

11. A Summary of Resignations and Dismissals, during the most recent fiscal year or during the current fiscal year up to the date of printing

of the annual report, of Persons Connected with The Company's Financial Report (Including The Chairman of The Board of Directors,

General Manager, Principal Accounting Officer, and Chief Internal Auditor) :

Item Resolution

Type of personnel changed Principal Accounting Officer

Date of board meeting 2009/04/30 (Effective date)

Name and title of the replaced person Clement Lin, Director of Finance and Accounting Division

Name and title of the replacement James Chen, Controller of Finance and Accounting Division

Reason for the change For job rotation

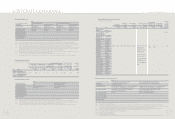

III. INFORMATION ON CPA PROFESSIONAL FEES :

1. Scale of Information on CPA professional fees

Accounting Firm Name of CPA Audit Period Note

Deloitte & Touche Ming-Hsien Yang Kwan-Chung Lai Nine Months Ended September 30, 2009

Ming-Hsien Yang Tze-Chun Wang Years Ended December 31, 2009 Due to adjustments in the managerial organization at Deloitte & Touche, the certifying PAs

have been changed from Ming-Hsien Yang CPA and Kwan-Chung Lai CPA to

Ming-Hsien Yang CPA and Tze-Chun Wang CPA.

Unit:NT$ thousands

Item

Scale of Fee Audit Fee Non-Audit Fee Total Fee

Under NT$ 2,000,000

NT$ 2,000,000 ~ NT$ 4,000,000

NT$ 4,000,000 ~ NT$ 6,000,000

NT$ 6,000,000 ~ NT$ 8,000,000

NT$ 8,000,000 ~ NT$ 10,000,000

√

Over NT$ 10,000,000

√√

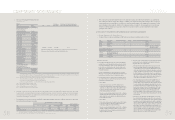

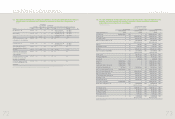

2. Information on CPA professional fees

> When non-audit fees paid to the certified public accountant, to the accounting firm of the certified public accountant, and/or to any affiliated enterprise

of such accounting firm are equivalent to one quarter or more of the audit fees paid thereto, the amounts of both audit and non-audit fees as well as

details of non-audit services shall be disclosed

Non-Audit Fee

System Company Human Others

Accounting Firm Name of CPA Audit Fee Design Registration Resource (note 1) Subtotal CPA's Audit Period Note

Ming-Hsien Yang Nine Months Ended Transfer pricing report,

Deloitte & Touche Kwan-Chung Lai 9,060 - 168 - 21,242 21,410 September 30, 2009 international tax

Ming-Hsien Yang Years Ended consultation, review of

Tze-Chun Wang December 31, 2009 shareholders' meeting

annual report, project

consultation and CPA

opinion on earnings

capitalization.

Note 1: Please record non-audit fees separately according to service item. If non-audit fees indicated under "Other" constitute 25 percent of total non-audit fees, the nature of those service items shall be

indicated in the Remarks column.

> When the company changes its accounting firm and the audit fees paid for the fiscal year in which such change took place are lower than those for the pre-

vious year, the reduction in the amount of audit fees, reduction percentage, and reason(s) therefor shall be disclosed.

HTC did not change its accounting firm.

> When the audit fees paid for the current year are lower than those for the previous fiscal year by 15 percent or more, the reduction in the amount of audit

fees, reduction percentage, and reason(s) therefor shall be disclosed.

The audit fees paid for the current year are not lower than those for the previous fiscal year by 15 percent, and, therefore, there is no further explanation.

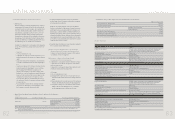

IV. INFORMATION ON REPLACEMENT OF CERTIFIED PUBLIC ACCOUNTANT: IF THE COMPANY HAS REPLACED

ITS CERTIFIED PUBLIC ACCOUNTANT WITHIN THE LAST TWO FISCAL YEARS OR ANY SUBSEQUENT INTER-

IM PERIOD, IT SHALL DISCLOSE THE FOLLOWING INFORMATION

1. Regarding the former certified public accountant

Date of replacement 12/28/2009

Reason for replacement and specifying such reason Due to adjustments in the managerial organization at Deloitte & Touche, the

certifying CPAs have been changed from Ming-Hsien Yang CPA and

Kwan-Chung Lai CPA to Ming-Hsien Yang CPA and Tze-Chun Wang CPA.

Specifying whether it was the certified public accountant that Concerned Person

voluntarily ended the engagement or declined further engagement Condition Accountant Appointer

voluntarily ended the engagement - -

discontinued the engagement. - -

Issued an audit report expressing other than an unqualified opinion None

during the two most recent years, furnish the opinion and reason.

Indicate whether there was any disagreement between the company and Yes Accounting principles or practices

the former certified public accountant Financial report disclosure

Auditing scope or procedure

Other

No √

Description

Disclose the information (Other matters required for disclosure under None

Article 10, subparagraph 5, item 1, point 4 of the Regulations Governing

Information to be Published in Annual Reports of Public Companies).

2. Regarding the successor certified public accountant

Name of the accounting firm Deloitte & Touche

Name of the certified public accountant Ming-Hsien Yang, Tze-Chun Wang

Date of engagement 12/28/2009

If prior to the formal engagement of the successor certified public accountant, the company consulted the None

newly engaged accountant regarding the accounting treatment of or application of accounting principles to a

specified transaction, or the type of audit opinion that might be rendered on the company's financial report,

the company shall state and identify the subjects discussed during those consultations and the consultation results.

The company shall consult and obtain written views from the successor certified public accountant regarding the None

the successor certified public accountant regarding the former certified public accountant, and shall make

disclosure thereof.

3. Response letter from the former CPA regarding the matters under Article 10, subparagraph 5, item 1, and Article 10, subparagraph 5, item

2, of these the Regulations Governing Information to be Published in Annual Reports of Public Companies.

None

V. WHERE THE COMPANY'S CHAIRPERSON, GENERAL MANAGER, OR ANY MANAGERIAL OFFICER IN CHARGE

OF FINANCE OR ACCOUNTING MATTERS HAS IN THE MOST RECENT YEAR HELD A POSITION AT THE

ACCOUNTING FIRM OF ITS CERTIFIED PUBLIC ACCOUNTANT OR AT AN AFFILIATED ENTERPRISE OF SUCH

ACCOUNTING FIRM, THE NAME AND POSITION OF THE PERSON, AND THE PERIOD DURING WHICH THE

POSITION WAS HELD, SHALL BE DISCLOSED.

None