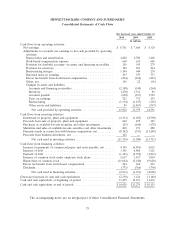

HP 2010 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2010 HP annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

|

|

HEWLETT-PACKARD COMPANY AND SUBSIDIARIES

Notes to Consolidated Financial Statements (Continued)

Note 1: Summary of Significant Accounting Policies (Continued)

HP limits the amount of revenue recognition for delivered elements to the amount that is not

contingent on the future delivery of products or services, future performance obligations or subject to

customer-specified return or refund privileges.

HP evaluates each deliverable in an arrangement to determine whether they represent separate

units of accounting. A deliverable constitutes a separate unit of accounting when it has standalone

value and there are no customer-negotiated refund or return rights for the delivered elements. If the

arrangement includes a customer-negotiated refund or return right relative to the delivered item and

the delivery and performance of the undelivered item is considered probable and substantially in HP’s

control, the delivered element constitutes a separate unit of accounting. In instances when the

aforementioned criteria are not met, the deliverable is combined with the undelivered elements and the

allocation of the arrangement consideration and revenue recognition is determined for the combined

unit as a single unit. Allocation of the consideration is determined at arrangement inception on the

basis of each unit’s relative selling price.

HP establishes VSOE of selling price using the price charged for a deliverable when sold

separately and, in rare instances, using the price established by management having the relevant

authority. TPE of selling price is established by evaluating largely similar and interchangeable

competitor products or services in standalone sales to similarly situated customers. The best estimate of

selling price is established considering internal factors such as margin objectives, pricing practices and

controls, customer segment pricing strategies and the product life cycle. Consideration is also given to

market conditions such as competitor pricing strategies and industry technology life cycles.

For fiscal 2008, pursuant to the previous guidance for revenue arrangements with multiple

deliverables prior to the adoption of Accounting Standards Update (‘‘ASU’’) No. 2009-13, ‘‘Multiple

Deliverable Revenue Arrangements,’’ for a sales arrangement with multiple elements, HP allocated

revenue to each element based on its relative fair value, or for software, based on VSOE of fair value.

In the absence of fair value for a delivered element, HP first allocated revenue to the fair value of the

undelivered elements and the residual revenue to the delivered elements. Where the fair value for an

undelivered element could not be determined, HP deferred revenue for the delivered elements until

the undelivered elements were delivered or the fair value was determinable for the remaining

undelivered elements. If the revenue for a delivered item was not recognized because it was not

separable from the undelivered item, then HP also deferred the cost of the delivered item. HP limited

the amount of revenue recognition for delivered elements to the amount that was not contingent on

the future delivery of products or services, future performance obligations or subject to customer-

specified return or refund privileges. For the purposes of income statement classification of products

and services revenue, when HP could not determine fair value for all of the elements in an

arrangement and the transaction was accounted for as a single unit of accounting, HP allocated

revenue to products and services based on a rational and consistent methodology. This methodology

utilized external and internal pricing inputs to derive HP’s best estimate of fair value for the elements

in the arrangement.

In instances when revenue is derived from sales of third-party vendor services, revenue is recorded

at gross when HP is a principal to the transaction and net of costs when HP is acting as an agent

between the customer and the vendor. Several factors are considered to determine whether HP is an

agent or principal, most notably whether HP is the primary obligor to the customer, has established its

own pricing, and has inventory and credit risks.

78