Google 2011 Annual Report Download - page 96

Download and view the complete annual report

Please find page 96 of the 2011 Google annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

recorded or as interest and other income, net, if the hedged transaction becomes probable of not occurring.

Further, we exclude the change in the time value of the options from our assessment of hedge effectiveness. We

record the premium paid or time value of an option on the date of purchase as an asset. Thereafter, we recognize

any change to this time value in interest and other income, net.

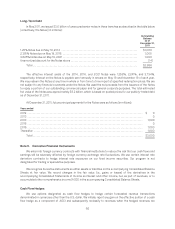

At December 31, 2011, the effective portion of our cash flow hedges before tax effect was $154 million, of

which $127 million is expected to be reclassified from AOCI to revenues within the next 12 months.

The notional principal of foreign exchange contracts to purchase U.S. dollars with Euros was €3.0 billion (or

approximately $4.1 billion) and €2.8 billion (or approximately $3.8 billion) at December 31, 2010 and December 31,

2011; the notional principal of foreign exchange contracts to purchase U.S. dollars with British pounds was

£1.5 billion (or approximately $2.3 billion) and £1.4 billion (or approximately $2.2 billion) at December 31, 2010 and

December 31, 2011; and the notional principal of foreign exchange contracts to purchase U.S. dollars with

Canadian dollars was C$407 million (or approximately $382 million) and C$504 million (or approximately $490

million) at December 31, 2010 and December 31, 2011. These foreign exchange contracts have maturities of 36

months or less.

Fair Value Hedges

We use forward contracts designated as fair value hedges to hedge foreign currency risks for our investments

denominated in currencies other than the U.S. dollar. Gains and losses on these contracts are recognized in

interest and other income, net, along with the offsetting losses and gains of the related hedged items. We exclude

changes in the time value for forward contracts from the assessment of hedge effectiveness and recognize them

in interest and other income, net. The notional principal of foreign exchange contracts to purchase U.S. dollars with

foreign currencies was $787 million and $1.0 billion at December 31, 2010 and December 31, 2011.

Other Derivatives

Other derivatives not designated as hedging instruments consist of forward and option contracts that we use

to hedge intercompany transactions and other monetary assets or liabilities denominated in currencies other than

the local currency of a subsidiary. We recognize gains and losses on these contracts as well as the related costs in

interest and other income, net, along with the gains and losses of the related hedged items. The notional principal

of foreign exchange contracts to purchase U.S. dollars with foreign currencies was $1.0 billion and $2.3 billion at

December 31, 2010 and December 31, 2011. The notional principal of foreign exchange contracts to sell U.S. dollars

for foreign currencies was $84 million and $472 million at December 31, 2010 and December 31, 2011. The

notional principal of foreign exchange contracts to purchase Euros with other foreign currencies was €991 million

(or approximately $1.3 billion) and €711 million (or approximately $929 million) at December 31, 2010 and

December 31, 2011. The notional principal of foreign exchange contracts to sell Euros for other foreign currencies

was €6 million (or approximately $8 million) at December 31, 2010 and no such contracts were outstanding at

December 31, 2011.

We also use exchange-traded interest rate futures contracts and “To Be Announced” (TBA) forward purchase

commitments of mortgage-backed assets to hedge interest rate risks on certain fixed income securities. The TBA

contracts meet the definition of derivative instruments in cases where physical delivery of the assets is not taken

at the earliest available delivery date. Our interest rate futures and TBA contracts (together interest rate contracts)

are not designated as hedging instruments. We recognize gains and losses on these contracts as well as the

related costs in interest and other income, net. The gains and losses are generally economically offset by

unrealized gains and losses in the underlying available-for-sale securities, which are recorded as a component of

AOCI until the securities are sold or other-than-temporarily impaired, at which time the amounts are moved from

AOCI into interest and other income, net. As of December 31, 2011, the total notional amounts of interest rate

contracts outstanding were $100 million.

67