Google 2011 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2011 Google annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

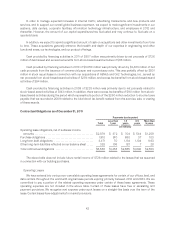

December 31, 2011, the notional principal and fair value of foreign exchange contracts to purchase U.S. dollars with

Euros were €2.8 billion (or approximately $3.8 billion) and $232 million; the notional principal and fair value of

foreign exchange contracts to purchase U.S. dollars with British pounds were £1.4 billion (or approximately $2.2

billion) and $80 million; and the notional principal and fair value of foreign exchange contracts to purchase U.S.

dollars with Canadian dollars were C$504 million (or approximately $490 million) and $17 million. These foreign

exchange contracts have maturities of 36 months or less. We may enter into similar contracts in other foreign

currencies in the future.

We considered the historical trends in currency exchange rates and determined that it was reasonably

possible that changes in exchange rates of 20% for our foreign currencies instruments could be experienced in the

near term.

If the U.S. dollar weakened by 20%, the amount recorded in AOCI before tax effect would have been

approximately $140 million and $132 million lower at December 31, 2010 and 2011, and the total amount of

expense recorded as interest and other income, net, would have been approximately $134 million and $138 million

higher in the years ended December 31, 2010 and 2011. If the U.S. dollar strengthened by 20%, the amount

recorded in accumulated AOCI before tax effect would have been approximately $1.2 billion higher at both

December 31, 2010 and 2011, and the total amount of expense recorded as interest and other income, net, would

have been approximately $175 million and $202 million higher in the years ended December 31, 2010 and 2011.

Transaction Exposure

Our exposure to foreign currency transaction gains and losses is the result of certain net receivables due from

our foreign subsidiaries and customers being denominated in currencies other than the functional currency of the

subsidiary, primarily the Euro and the British pound. Our foreign subsidiaries conduct their businesses in local

currency. We have entered into foreign exchange contracts to offset the foreign exchange risk on certain

monetary assets and liabilities denominated in currencies other than the local currency of the subsidiary.

The notional principal of foreign exchange contracts to purchase U.S. dollars with foreign currencies was $1.0

billion and $2.3 billion at December 31, 2010 and 2011. The notional principal of foreign exchange contracts to sell

U.S. dollars for foreign currencies was $84 million and $472 million at December 31, 2010 and December 31, 2011.

The notional principal of foreign exchange contracts to purchase Euros with other foreign currencies was

€991 million (or approximately $1.3 billion) and €711 million (or approximately $929 million) at December 31, 2010

and 2011. The notional principal of foreign exchange contracts to sell Euros for other foreign currencies was

€6 million (or approximately $8 million) at December 31, 2010 and no such contracts were outstanding at

December 31, 2011.

We considered the historical trends in currency exchange rates and determined that it was reasonably

possible that adverse changes in exchange rates of 20% for all currencies could be experienced in the near term.

These changes would have resulted in an adverse impact on income before income taxes of approximately $20

million and $27 million at December 31, 2010 and 2011. The adverse impact at December 31, 2010 and 2011 is after

consideration of the offsetting effect of approximately $467 million and $503 million from foreign exchange

contracts in place for the months of December 2010 and December 2011. These reasonably possible adverse

changes in exchange rates of 20% were applied to total monetary assets and liabilities denominated in currencies

other than the local currencies at the balance sheet dates to compute the adverse impact these changes would

have had on our income before income taxes in the near term.

Interest Rate Risk

We invest our excess cash primarily in highly liquid debt instruments of the U.S. government and its agencies,

municipalities in the U.S., debt instruments issued by foreign governments, time deposits, money market and other

funds, mortgage-backed securities, and corporate debt securities. By policy, we limit the amount of credit

exposure to any one issuer.

46