Dollar General 2012 Annual Report Download - page 127

Download and view the complete annual report

Please find page 127 of the 2012 Dollar General annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

|

|

10-K

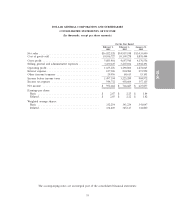

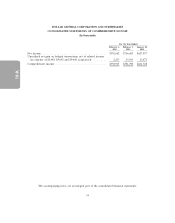

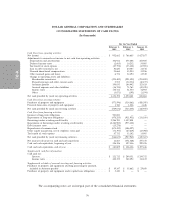

Contingent Liabilities—Income Taxes. Income tax reserves are determined using the methodology

established by accounting standards relating to uncertainty in income taxes. These standards require

companies to assess each income tax position taken using a two-step process. A determination is first

made as to whether it is more likely than not that the position will be sustained, based upon the

technical merits, upon examination by the taxing authorities. If the tax position is expected to meet the

more likely than not criteria, the benefit recorded for the tax position equals the largest amount that is

greater than 50% likely to be realized upon ultimate settlement of the respective tax position.

Uncertain tax positions require determinations and estimated liabilities to be made based on provisions

of the tax law which may be subject to change or varying interpretation. If our determinations and

estimates prove to be inaccurate, the resulting adjustments could be material to our future financial

results.

Contingent Liabilities—Legal Matters. We are subject to legal, regulatory and other proceedings

and claims. We establish liabilities as appropriate for these claims and proceedings based upon the

probability and estimability of losses and to fairly present, in conjunction with the disclosures of these

matters in our financial statements and SEC filings, management’s view of our exposure. We review

outstanding claims and proceedings with external counsel to assess probability and estimates of loss,

which includes an analysis of whether such loss estimates are probable, reasonably possible, or remote.

We re-evaluate these assessments on a quarterly basis or as new and significant information becomes

available to determine whether a liability should be established or if any existing liability should be

adjusted. The actual cost of resolving a claim or proceeding ultimately may be substantially different

than the amount of the recorded liability. In addition, because it is not permissible under U.S. GAAP

to establish a litigation liability until the loss is both probable and estimable, in some cases there may

be insufficient time to establish a liability prior to the actual incurrence of the loss (upon verdict and

judgment at trial, for example, or in the case of a quickly negotiated settlement).

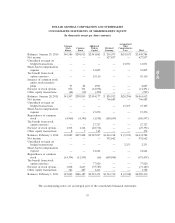

Lease Accounting and Excess Facilities. Many of our stores are subject to build-to-suit

arrangements with landlords, which typically carry a primary lease term of 10-15 years with multiple

renewal options. We also have stores subject to shorter-term leases and many of these leases have

renewal options. Certain of our stores have provisions for contingent rentals based upon a percentage

of defined sales volume. We recognize contingent rental expense when the achievement of specified

sales targets is considered probable. We recognize rent expense over the term of the lease. We record

minimum rental expense on a straight-line basis over the base, non-cancelable lease term commencing

on the date that we take physical possession of the property from the landlord, which normally includes

a period prior to store opening to make necessary leasehold improvements and install store fixtures.

When a lease contains a predetermined fixed escalation of the minimum rent, we recognize the related

rent expense on a straight-line basis and record the difference between the recognized rental expense

and the amounts payable under the lease as deferred rent. Tenant allowances, to the extent received,

are recorded as deferred incentive rent and amortized as a reduction to rent expense over the term of

the lease. We reflect as a liability any difference between the calculated expense and the amounts

actually paid. Improvements of leased properties are amortized over the shorter of the life of the

applicable lease term or the estimated useful life of the asset.

For store closures (excluding those associated with a business combination) where a lease

obligation still exists, we record the estimated future liability associated with the rental obligation on

the date the store is closed in accordance with accounting standards for costs associated with exit or

disposal activities. Based on an overall analysis of store performance and expected trends, management

periodically evaluates the need to close underperforming stores. Liabilities are established at the point

of closure for the present value of any remaining operating lease obligations, net of estimated sublease

income, and at the communication date for severance and other exit costs. Key assumptions in

calculating the liability include the timeframe expected to terminate lease agreements, estimates related

to the sublease potential of closed locations, and estimation of other related exit costs. Historically,

48