Cigna 2009 Annual Report Download - page 105

Download and view the complete annual report

Please find page 105 of the 2009 Cigna annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

|

|

85

In those cases, the Company expects to have the flexibility to satisfy liquidity needs through a variety of measures, including

intercompany borrowings and sales of liquid investments. The parent company may borrow up to $400 million from CGLIC without

prior state approval. In addition, the Company may use short-term borrowings, such as the commercial paper program and the

committed line of credit agreement of up to $1.75 billion subject to the maximum debt leverage covenant in its line of credit

agreement. As of December 31, 2009, the Company had an additional $1.5 billion of borrowing capacity within the maximum debt

leverage covenant in the line of credit agreement in addition to the $2.5 billion of debt outstanding.

Though the Company believes it has adequate sources of liquidity, significant disruption or volatility in the capital and credit markets

could affect the Company’s ability to access those markets for additional borrowings or increase costs associated with borrowing

funds.

Solvency regulation. Many states have adopted some form of the National Association of Insurance Commissioners (“NAIC”) model

solvency-related laws and risk-based capital rules (“RBC rules”) for life and health insurance companies. The RBC rules recommend

a minimum level of capital depending on the types and quality of investments held, the types of business written and the types of

liabilities incurred. If the ratio of the insurer's adjusted surplus to its risk-based capital falls below statutory required minimums, the

insurer could be subject to regulatory actions ranging from increased scrutiny to conservatorship.

In addition, various non-U.S. jurisdictions prescribe minimum surplus requirements that are based upon solvency, liquidity and

reserve coverage measures. During 2009, the Company’s HMOs and life and health insurance subsidiaries, as well as non-U.S.

insurance subsidiaries, were compliant with applicable RBC and non-U.S. surplus rules.

Effective December 31, 2009 the Company’s principal life insurance subsidiary, CGLIC, implemented the NAIC’s Actuarial

Guideline XLIII (also known as AG 43 or VACARVM), which is applicable to CGLIC’s statutory reserves for GMDB and GMIB

contracts totaling $1.6 billion as of December 31, 2009. As provided under this guidance, CGLIC received approval from the State of

Connecticut to grade-in the full effect of the guideline over a 3-year period. Accordingly, upon implementation at December 31,

2009, statutory surplus for CGLIC was reduced by $40 million. If the guidance had been fully implemented at December 31, 2009,

statutory surplus would have been reduced by $110 million. Management does not anticipate that this implementation will have a

material impact on the amount of dividends expected to be paid by CGLIC to the parent company in 2010. This implementation has

no impact on measurement of the Company’s results of operations or financial condition as determined under GAAP.

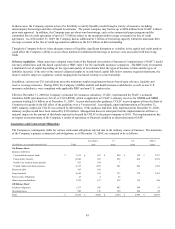

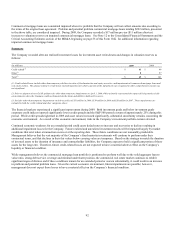

Guarantees and Contractual Obligations

The Company is contingently liable for various contractual obligations entered into in the ordinary course of business. The maturities

of the Company’s primary contractual cash obligations, as of December 31, 2009, are estimated to be as follows:

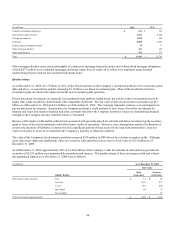

Less than 1 1-3 4-5 After 5

(In millions, on an undiscounted basis) Total year years years years

On-Balance Sheet:

Insurance liabilities:

Contractholder deposit funds $ 7,613 $ 667 $ 840 $ 769 $ 5,337

Future policy benefits 11,040 452 852 860 8,876

Health Care medical claims payable 921 914 7 - -

Unpaid claims and claims expenses 4,315 1,292 941 606 1,476

Short-term debt 103 103 - - -

Long-term debt 4,620 168 753 278 3,421

Non-recourse obligations 25 2 23 - -

Other long-term liabilities 1,355 617 218 134 386

Off-Balance Sheet: 1

Purchase obligations 1,173 495 483 144 51

Operating leases 500 116 190 104 90

Total $ 31,665 $ 4,826 $ 4,307 $ 2,895 $ 19,637