BMW 2006 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2006 BMW annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

|

|

43

Analysis of the Group Financial Statements

Group internal management system

The underlying long-term objective of the group’s

internal management system is to increase the value

of the BMW Group as a whole. The targets set for

the Automobiles, Motorcycles and Financial Services

segments all stem from this objective. Within the Au-

tomobiles and Motorcycles segments, this approach

is put into practise for specific product, process and

structure-related projects. By contrast, the Financial

Services segment is primarily concerned with the

cash flows resulting from its credit and lease portfolio.

Minimum rate of return derived from cost of

capital

The cornerstone of the value-added management

of the BMW Group is the entity-specific minimum

rate of return, derived from capital market data, and

based on the weighted average cost of capital:

Cost of equity capital x market value of equity capital

Market value of equity and debt capital

WACC = +

Cost of debt capital x market value of debt capital

Market value of equity and debt capital

The cost of equity capital is measured using the

Capital Asset Pricing Model (CAPM). The cost of

debt capital is partly based on the average interest

rate paid for long-term external debt and partly on

the interest rate applicable for pension obligations.

Value management in the context of project

control

The strategies set for each segment (and also the

ensuing project decisions) give rise to the areas of

strategic emphasis which are then implemented at

a functional level. The overall project development

process becomes more targeted as a result of the

closer link between the strategies defined for each

segment and the objectives defined for specific

projects. Once a project decision has been reached,

the task is to manage each individual project over

time. This involves the continual monitoring of

projects as well as determining and implementing

measures necessary to achieve the defined targets.

The project decision and related project selec-

tion are therefore important aspects of value-based

management. Net present values (NPVs) and rates of

return are computed as part of the decision-making

process. This involves computing the present value

of cash flows and the internal project rate of return

(or model rate of return in the case of vehicle projects)

expected to be generated by a project decision and

comparing them with the minimum rate of return

derived from capital market data.

Using this method,the amount by which aproject

will contribute to the total value of the segment

(i.e. the project’s added-value) can be documented

when the project decision is taken. Targets and per-

formance are each controlled using target NPVs and

individual cash flow-related parameters which have

an impact on those values.

The NPV of a project programme is computed

by aggregating the amounts for all projects and dis-

counting them back to a specific date. This value

serves as the main target for the Automobiles and

Motorcycles segments. The business value of each

segment is then computed by deducting the market

value of debt capital. For both of these segments,

the objective is to increase business value, as com-

puted above, on a continuous basis.

Return on capital used to measure value on

a periodic basis

The management of product projects and product

programmes described above is subject to basic

conditions which result from periodic planning.The

aim here is to monitor and manage periodic tar-

gets

on a long-term basis. Periodic performance is

managed in the light of defined accounting policies

and external financial reporting requirements.The

BMW Group primarily uses profit before tax and

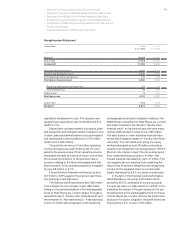

Key performance indicators 2006 2005 2004*2003 2002

in %

*adjusted for new accounting treatment of pension obligations

Return on Capital Employed

Automobiles 21.7 23.2 25.4 23.8 30.1

Motorcycles 17.7 17.8 10.4 16.7 22.3

Return on Assets

Financial Services 1.4 1.3 1.4 1.4 1.4

BMW Group 6.3 5.6 6.5 6.6 7.6